❔ Futures Questions and Answers

❔ How do you calculate your percentage profit or loss on a trade?

✔ Conceptually, leverage is always the amount of money at stake divide by the amount of money you had to “put down.” In this case, you “put down” your money by depositing the initial margin in the margin account. Therefore, we will use the initial amount we put into our margin account as the denominator of our leverage formula.

✏️ Suppose a manufacturer purchases a soybean contract and then the price drops by . Their initial margin was . What is their percentage loss?

✔ Click here to view answer

The contract size is bushels, so they have lost . Their initial investment was . You can calculate their percent loss by dividing their dollar loss by their initial investment:

There are many strike prices in options, but only one futures contract price.

With options, supply and demand determine the premium. With futures, supply and demand determine the futures contract price.

❔ How are futures used for hedging? (the Farmer and the Miller)

✔ The original use for forwards was as a way to manage risk from volatile commodity prices (ie hedging commodity price risk). Imagine you are a farmer growing a single crop such as wheat. Your entire annual revenue depends critically on the highly volatile market price of wheat. If the price is too low, you could go bankrupt and be forced to sell all of your assets at fire-sale prices in order to pay back your debts.

On the flip side, imagine a miller who sells flour to bakeries. The miller faces a risk management problem that is the mirror image of the farmer’s problem. If the price of wheat is too low, the miller might have to raise their prices and lose customers.

Both the farmer and the miller can remove all price risk by locking in the prices early using futures contracts. Then they don’t need to worry what the final price is at harvest time. The farmer will sell the futures contract, locking in a price to sell their wheat and the miller will buy the futures contract, locking in a price to buy the wheat.

No money need change hands at this time. The futures contract is just a standardized agreement to buy and sell a specified quantity of the commodity at a specific time in the future. It’s a win-win situation because it protects both the buyer and the seller from future price fluctuations.

You can think of this as the original “killer app” for futures markets. As a result of the popularity of agricultural futures, most US futures markets are located in the Midwest - most notably in Chicago.

❔ What are the “futures price” and the “contract price?” How are they determined? What does “the contract closed at” mean?

✔ The “futures price” and the “contract price” are different words for the same thing.

As you know, a futures contract is based on the idea of purchasing a specific good on a specific day in the future. Jargon:

Consider the phrase, “Suppose that on June 27, the gold futures contract for August delivery closed at per ounce.”

The contract price is the price you lock in when you buy the contract or sell the contract. If you “bought” the contract, then you have committed to buy ounces of gold for a locked-in “futures price” (aka contract price) of . On the other hand, if you sold the contract, you have committed to sell the gold at that price. Saying that the “contract closed” at means that the final price on June 27 was . Closing prices for futures contracts are also important because they are used for setting margin requirements.

❔ How is the price of a futures contract decided?

✔ As discussed above, the price in a futures contract is known as the “contract price.” It is decided by supply and demand, just like in HES Econ E1000, Essentials of Economics. In a securities market, supply and demand are represented by the orders (such as limit orders) at the exchange. See also: 🔎 Limit orders and how modern markets actually work. Option premiums are determined in the same way. (If you are curious to learn more about supply and demand, Bruce and I teach E1000 every semester.)

❔ How do we interpret leverage?

✔ When Bruce described leverage, he said that with leverage, dollar invested is comparable to dollars of the underlying commodity or index.

For example, suppose the initial margin is on a soybean contract for bushels. If the price is , then the value of the contract is . The “amount at stake” is , but you only have to put up your initial margin of . Therefore, the margin is

The vital implication here is that if you are leveraged at , if you are speculating and the price of soybeans moves in your favor, then you will have a total return of . A tiny price movement turned into a huge return on your investment. However, a move in the other direction would have caused a loss! This leverage causes derivatives to be tremendously risky! The reason that Bruce focuses on leverage is so that you understand how risky these derivatives can be.

❔ If you “buy” the contract and hold it to expiration, who would you be buying the underlying good from?

✔ All that the exchange does is match buyers of the contract up with sellers of the contract, using an auction process. Whenever you buy the contract, there is also a seller of the contract. If you hold the contract to expiration, you will essentially be matched up with a seller of the contract at that point. (I say essentially, because you will actually buy the good from the CME - however they will get the good from the seller of the contract that you are matched with.) There will always be the same number of buyers of the contract and sellers of the contract, just as there will always be the same number of long calls as there are of short calls. It’s a consequence of the way that buyers and sellers are matched up by the market.

❔ Brain-food questions

Some of the questions asked during section require a deeper understanding of how futures work on a concrete, moment to moment basis. These FAQs lay out a foundation for this understanding.

🧠 How does short-term Futures Trading work?

As described above, the futures price is determined on the exchange much like a stock price or an option premium is determined. It changes throughout the day, constantly, so there is always a price for a given contract that you can buy or sell the contract for.* This contract changes throughout the day as shown in the following diagram:

*More precisely, as we discussed in section when we were covering stocks and options, there is always a bid, an ask, and a last price - however, for simplicity, because the bid and ask are very close, we will just assume that there is one price that you can buy or sell the contract for.

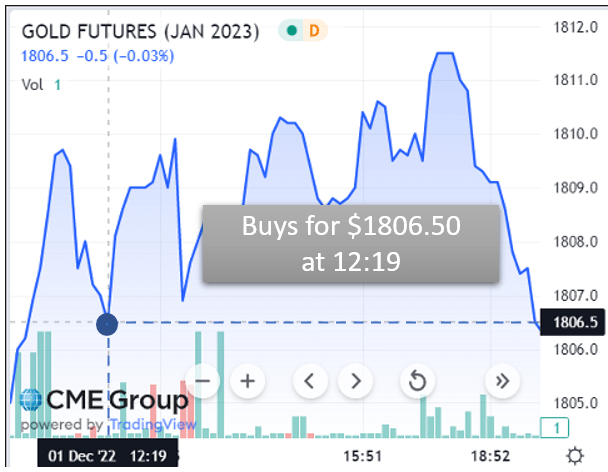

Imagine that Daisy is a short-term futures trader. At 12:19 PM, she buys the January contract at . Legally, this means that she has obligated herself to purchase ounces of gold for . However, Daisy is a day trader, so she knows that she will exit this trade by the end of the day by submitting an offsetting trade.

Daisy

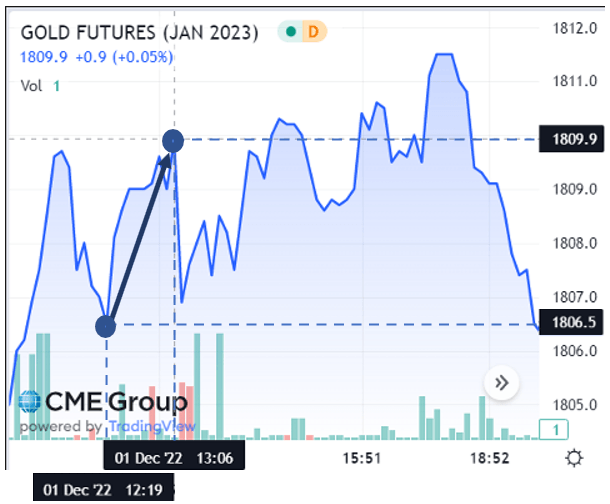

As it happens, Daisy exits the trade at 1:06 PM by submitting an offsetting trade to the exchange. This just means that she sells the exact same contract that she bought early. She just submits a sell order for the exact same contract (rather than a buy order). Let’s suppose that her order is filled at 1:06 PM (ie 13:06 in 24-hour time) for .

At this point, Daisy is obligated to, on the date of contract expiration, buy ounces of gold for and sell ounces of gold for .

✏️ What will Daisy’s profit be on the expiration date?

✔ Click here to view answer

She will buy the gold for and sell it for per ounce. This is a per-ounce profit of

Because the contract size is ounces, she will make

To simplify life for Daisy, the CME will take over the process from here. On the expiration date, it will be the one to buy the gold for and sell it for . In fact, based on these future profits, it can cash her out right now, depositing in her account.

❔ How does the CME implement Daisy’s exit from her trade?

✔ To implement this, the CME will essentially match up the traders on the opposite side of Daisy’s trades.

Suppose that in the auction in which Daisy bought the future, the person on the other side of the trade was named Rob. Suppose, similarly, that when Daisy sold the future, the person on the other side of the trade was named Pierre:

| Daisy | On the other side of the trade | |

|---|---|---|

| 12:19 PM | Daisy is obligated to buy at → | ← Rob is obligated to sell at |

| 1:06 PM | Daisy is obligated to sell at → | ← Pierre is obligated to buy at |

At expiration, the CME will essentially match up Rob with Pierre. Specifically, the CME will buy the gold from Rob for and sell the gold to Pierre at , pocketing a profit of per ounce. This will compensate the CME for the that it paid out to Daisy when she closed her trade.

| Daisy | On the other side of the trade | |

|---|---|---|

| 12:19 PM | Daisy is obligated to buy at | ↓Rob is obligated to sell at |

| 1:06 PM | Daisy is obligated to sell at | ↑Pierre is obligated to buy at |

In the end, every single trader that holds a contract to expiration will either buy or sell from the CME. In other words, the CME will be everyone’s counterparty. However, the CME’s business model is based on not taking risks. By matching counterparties up as described above, the CME can hedge their own risks.

❔ What is Marking to Market?

✔ For cash settled contracts, your margin account is adjusted every day based on the closing contract price that day. This is known as “marking to market.” It is how the exchange guarantees that you always have enough money in your margin account. It also allows you to access some of your gains before the contract expires or you close your position.

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.