✏️ Construct a table for a bear spread

✏️ If the TSLA 28 call is selling for $2, and the TSLA 29 call is selling for $1.50, construct a bear spread using these nearby $28 and $29 calls. Construct a table like the ones we did in class showing profit and loss at relevant stock prices for each part of the spread, and the net profit or loss for the entire spread position. Be sure to show the stock price at which the spread has its maximum gain, its maximum loss, and just breaks even.

We will start with the table from the slide:

| 0 | 600 | 605 | 610 | 615 | 620 | 630 | |

|---|---|---|---|---|---|---|---|

| Short GOOG 600 call @ 10 | |||||||

| Long GOOG 610 call @ 5 | |||||||

| Net Profit/Loss from Position |

The first thing we need to do is figure out which options you buy and/or sell to construct the bear spread. I have cheat sheets you can look up for doing this on the following page: 👨🏫 Notes on Lecture 12 Here is the relevant portion:

📖 For reference: how to construct spreads

Section titled “📖 For reference: how to construct spreads”- A bull spread is made of a long call and a short call with different strike prices. The strike prices match the two kinks in the diagram. The lower strike price is for the long call.

- A bear spread is made of a long call and a short call with different strike prices. The lower strike price is for the short call.**

We want to make a bear spread from these nearby $28 and $29 calls, so we will sell (short) a 28 call and we will buy (long) a 29 call.

| Short/Sell TSLA 28 call @ 2 | |||||||

| Long/Buy TSLA 29 call @ 1.50 | |||||||

| Net Profit/Loss from Position |

Next, we need to choose the stock prices. Bruce says, “be sure to show the stock price at which the spread has its maximum gain, its maximum loss, and just breaks even.”

| 0 | 26 | 28 | 28.5 | 29 | 30 | |

|---|---|---|---|---|---|---|

| Short/Sell TSLA 28 call @ 2 | ||||||

| Long/Buy TSLA 29 call @ 1.50 | ||||||

| Net Profit/Loss from Position |

I chose to include S=$0 because it’s an interesting what happens if TSLA goes to $0.

I chose 26 because it is below the lower strike price.

I chose 28 because it is the lower strike price.

I chose 28.5 because it is between the strike prices and I’m hoping it will be the breakeven point.

I chose 29 because it is the higher strike price.

I chose 30 because it is higher than the higher strike price.

After that, we just fill in the profit or loss from the two options and the Net Profit/Loss from the position like Bruce did in class. See below if you aren’t sure how to calculate the Profit and Loss numbers. We focused very heavily on calculating profit and loss for individual options in the sections after lecture 11. See also ✏️ Intro to Options and 🔎 Solutions for all 8 types of P/L problems

| 0 | 26 | 28 | 28.5 | 29 | 30 | 32 | |

|---|---|---|---|---|---|---|---|

| Short TSLA 28 call @ 2 | $2 | $2 | $2 | $1.50 | $1 | $0 | -$2 |

| Long TSLA 29 call @ 1.50 | -$1.50 | -$1.50 | -$1.50 | -$1.50 | -$1.50 | -$0.50 | $1.50 |

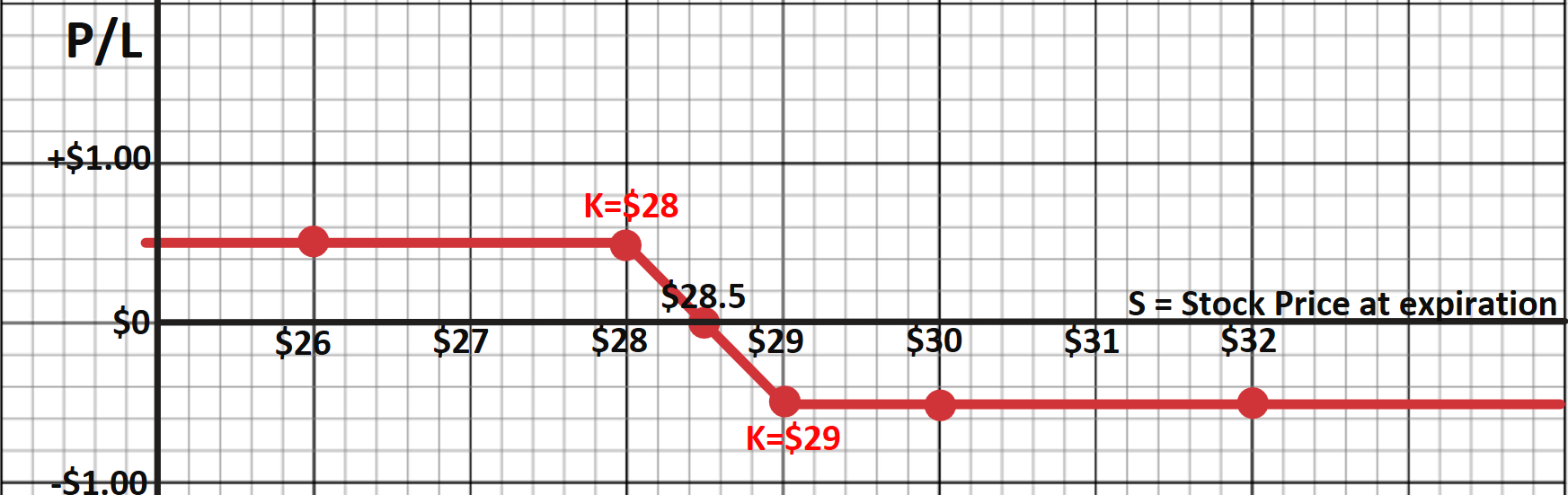

| Net Profit/Loss from Position | $0.50 | $0.50 | $0.50 | $0 | -$0.50 | -$0.50 | -$0.50 |

In the final row of the table above, for each stock price I’ve added the P/Ls for the two options to get the Net P/L from the position. For example, if S=28.5, I have a profit of $1.50 from the short call and a loss of $1.50 from the long call. Combining these, I just break even.

Finally, we can plot the Net Profit/Loss from Position. Each of the red dots in the following diagram is the Net P/L from one of the stock prices in the table. We can see that the characteristic P/L shape of a bear spread emerges:

Calculating the P/L for the Long K=$29 Call

Section titled “Calculating the P/L for the Long K=$29 Call”It is easier to calculate the P/L for a long call than it is to calculate the P/L for a short call. Therefore, we start with calculating the P/L for the Long TSLA 29 call @ 1.50. The details of how to calculate each of the following numbers are below.

| 0 | 26 | 28 | 28.5 | 29 | 30 | 32 | |

|---|---|---|---|---|---|---|---|

| Short TSLA 28 call @ 2 | |||||||

| Long TSLA 29 call @ 1.50 | -$1.50 | -$1.50 | -$1.50 | -$1.50 | -$1.50 | -$0.50 | $1.50 |

| Net Profit/Loss from Position |

Note: if you need general help on how to calculate the P/L on a long call (ie when you buy a call), see this page:🔎 Introduction to Options

When S=$0

Section titled “When S=$0”View the answer to the following problem to see how to calculate the P/L for a Long K=$29 Call @ $1.5 when S=$0

✏️ You have Bought a K=$29 Call. It is about to expire. Suppose S=$0 and Premium=$1.50.

- Will you exercise this option?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- Out of The Money, so WON'T be exercised.

- P/L = -$1.50.

Full Explanation:

This Long Call allows you to buy shares of stock worth S=$0 for K=$29.

You could easily purchase the stock on the open market for $0, so exercising the option would mean overpaying by $29. We would think of this as a per-share $29 loss.

Clearly, you won’t exercise the option, so it will just expire worthless. Because you can’t profitably exercise the option, we say the option is “Out of The Money (OTM)” and has no intrinsic value (IV=$0).

The only impact on your P/L is the $1.50 premium you paid. In hindsight, this money was wasted. P/L = -$1.50 (per share). Better luck next time!

When S=$26

Section titled “When S=$26”View the answer to the following problem to see how to calculate the P/L for a Long K=$29 Call @ $1.5 when S=$26

✏️ You have Bought a K=$29 Call. It is about to expire. Suppose S=$26 and Premium=$1.50.

- Will you exercise this option?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- Out of The Money, so WON'T be exercised.

- P/L = -$1.50.

Full Explanation:

This Long Call allows you to buy shares of stock worth S=$26 for K=$29.

You could easily purchase the stock on the open market for $26, so exercising the option would mean overpaying by $3. We would think of this as a per-share $3 loss.

Clearly, you won’t exercise the option, so it will just expire worthless. Because you can’t profitably exercise the option, we say the option is “Out of The Money (OTM)” and has no intrinsic value (IV=$0).

The only impact on your P/L is the $1.50 premium you paid. In hindsight, this money was wasted. P/L = -$1.50 (per share). Better luck next time!

When S=$28

Section titled “When S=$28”View the answer to the following problem to see how to calculate the P/L for a Long K=$29 Call @ $1.5 when S=$28

✏️ You have Bought a K=$29 Call. It is about to expire. Suppose S=$28 and Premium=$1.50.

- Will you exercise this option?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- Out of The Money, so WON'T be exercised.

- P/L = -$1.50.

Full Explanation:

This Long Call allows you to buy shares of stock worth S=$28 for K=$29.

You could easily purchase the stock on the open market for $28, so exercising the option would mean overpaying by $1. We would think of this as a per-share $1 loss.

Clearly, you won’t exercise the option, so it will just expire worthless. Because you can’t profitably exercise the option, we say the option is “Out of The Money (OTM)” and has no intrinsic value (IV=$0).

The only impact on your P/L is the $1.50 premium you paid. In hindsight, this money was wasted. P/L = -$1.50 (per share). Better luck next time!

When S=$28.50

Section titled “When S=$28.50”View the answer to the following problem to see how to calculate the P/L for a Long K=$29 Call @ $1.5 when S=$28.5

✏️ You have Bought a K=$29 Call. It is about to expire. Suppose S=$28.50 and Premium=$1.50.

- Will you exercise this option?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- Out of The Money, so WON'T be exercised.

- P/L = -$1.50.

Full Explanation:

This Long Call allows you to buy shares of stock worth S=$28.50 for K=$29.

You could easily purchase the stock on the open market for $28.50, so exercising the option would mean overpaying by $0.50. We would think of this as a per-share $0.50 loss.

Clearly, you won’t exercise the option, so it will just expire worthless. Because you can’t profitably exercise the option, we say the option is “Out of The Money (OTM)” and has no intrinsic value (IV=$0).

The only impact on your P/L is the $1.50 premium you paid. In hindsight, this money was wasted. P/L = -$1.50 (per share). Better luck next time!

When S=$29

Section titled “When S=$29”View the answer to the following problem to see how to calculate the P/L for a Long K=$29 Call @ $1.5 when S=$29

✏️ You have Bought a K=$29 Call. It is about to expire. Suppose S=$29 and Premium=$1.50.

- Will you exercise this option?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- At The Money, so WON'T be exercised.

- P/L = -$1.50.

Full Explanation:

This Long Call allows you to buy shares of stock worth S=$29 for K=$29.

You could easily purchase the stock on the open market for $29, so exercising the option would mean overpaying by $0. We would think of this as a per-share $0 loss.

Clearly, you won’t exercise the option, so it will just expire worthless. Because you can’t profitably exercise the option, we say the option is “Out of The Money (OTM)” and has no intrinsic value (IV=$0).

The only impact on your P/L is the $1.50 premium you paid. In hindsight, this money was wasted. P/L = -$1.50 (per share). Better luck next time!

When S=$30

Section titled “When S=$30”View the answer to the following problem to see how to calculate the P/L for a Long K=$29 Call @ $1.5 when S=$30

✏️ You have Bought a K=$29 Call. It is about to expire. Suppose S=$30 and Premium=$1.50.

- Will you exercise this option?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- In The Money, so WILL be exercised.

- P/L = -$0.50.

Full Explanation:

This Long Call allows you to buy shares of stock worth S=$30 for K=$29. A mnemonic is that you can “Call” the shares to you and someone else (your counterparty) will have to sell them to you for K=$29.

That is a discount of $1, so this option is “In The Money (ITM)” and you will exercise it. When you exercise it, you will gain $1. This $1 is the option's intrinsic value.

(If you don’t want to buy more shares, you could easily exercise the option to buy them for K=$29 and then turn around and sell them on the market for S=$30, netting a $1 profit. You could even take out a short-term loan to do this.)

In addition to the $1 gain, you also paid a premium of $1.50. Therefore, your final P/L combines the $1 gain and the $1.50 loss: P/L = $1 - $1.50 = -$0.50 (per share).

When S=$32

Section titled “When S=$32”View the answer to the following problem to see how to calculate the P/L for a Long K=$29 Call @ $1.5 when S=$32 ⇨ P/L = $1.50

✏️ You have Bought a K=$29 Call. It is about to expire. Suppose S=$32 and Premium=$1.50.

- Will you exercise this option?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- In The Money, so WILL be exercised.

- P/L = $1.50.

Full Explanation:

This Long Call allows you to buy shares of stock worth S=$32 for K=$29. A mnemonic is that you can “Call” the shares to you and someone else (your counterparty) will have to sell them to you for K=$29.

That is a discount of $3, so this option is “In The Money (ITM)” and you will exercise it. When you exercise it, you will gain $3. This $3 is the option's intrinsic value.

(If you don’t want to buy more shares, you could easily exercise the option to buy them for K=$29 and then turn around and sell them on the market for S=$32, netting a $3 profit. You could even take out a short-term loan to do this.)

In addition to the $3 gain, you also paid a premium of $1.50. Therefore, your final P/L combines the $3 gain and the $1.50 loss: P/L = $3 - $1.50 = $1.50 (per share).

Calculating the P/L for the Short K=$28 Call

Section titled “Calculating the P/L for the Short K=$28 Call”Next, we move on to calculate the P/L for the Short TSLA 28 call @ 2. The details of how to calculate each of the following numbers are below.

| 0 | 26 | 28 | 28.5 | 29 | 30 | 32 | |

|---|---|---|---|---|---|---|---|

| Short TSLA 28 call @ 2 | $2 | $2 | $2 | $1.50 | $1 | $0 | -$2 |

| Long TSLA 29 call @ 1.50 | |||||||

| Net Profit/Loss from Position |

Note: if you need general help on how to calculate the P/L on a short call (ie when you sell a call), see this page (and scroll down): 🔎 Introduction to Options

When S=$0

Section titled “When S=$0”View the answer to the following problem to see how to calculate the P/L for a Short K=$28 Call @ $2

✏️ You have Sold/Written a K=$28 Call. It is about to expire. Suppose S=$0 and Premium=$2.

- Will this option be exercised?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- Out of The Money, so WON'T be exercised.

- P/L = $2.

Full Explanation:

You have sold an option that obligates you to sell shares of stock worth S=$0 for K=$28 if requested.

You can think of yourself as being matched with a “counterparty” who purchased the option you wrote/sold. Just as you have a Short Call, they have a Long Call. They decide whether to exercise the Long Call they purchased. If they do, you must sell them 100 shares of the underlying stock for K=$28.

From your counterparty's perspective, there is no way to make money by paying $28 for shares only worth $0. Therefore, we say this option is “Out of The Money (OTM)” and has no intrinsic value (IV=$0).

Given this, your counterparty won’t exercise the option. The only impact on your P/L is the $2 premium your counterparty paid you. P/L = $2 (per share).

When S=$26

Section titled “When S=$26”View the answer to the following problem to see how to calculate the P/L for a Short K=$28 Call @ $2 when S=$26

✏️ You have Sold/Written a K=$28 Call. It is about to expire. Suppose S=$26 and Premium=$2.

- Will this option be exercised?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- Out of The Money, so WON'T be exercised.

- P/L = $2.

Full Explanation:

You have sold an option that obligates you to sell shares of stock worth S=$26 for K=$28 if requested.

You can think of yourself as being matched with a “counterparty” who purchased the option you wrote/sold. Just as you have a Short Call, they have a Long Call. They decide whether to exercise the Long Call they purchased. If they do, you must sell them 100 shares of the underlying stock for K=$28.

From your counterparty's perspective, there is no way to make money by paying $28 for shares only worth $26. Therefore, we say this option is “Out of The Money (OTM)” and has no intrinsic value (IV=$0).

Given this, your counterparty won’t exercise the option. The only impact on your P/L is the $2 premium your counterparty paid you. P/L = $2 (per share).

When S=$28

Section titled “When S=$28”View the answer to the following problem to see how to calculate the P/L for a Short K=$28 Call @ $2 when S=$28

✏️ You have Sold/Written a K=$28 Call. It is about to expire. Suppose S=$28 and Premium=$2.

- Will this option be exercised?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- At The Money, so WON'T be exercised.

- P/L = $2.

Full Explanation:

You have sold an option that obligates you to sell shares of stock worth S=$28 for K=$28 if requested.

You can think of yourself as being matched with a “counterparty” who purchased the option you wrote/sold. Just as you have a Short Call, they have a Long Call. They decide whether to exercise the Long Call they purchased. If they do, you must sell them 100 shares of the underlying stock for K=$28.

From your counterparty's perspective, there is no way to make money by paying $28 for shares only worth $28. Therefore, we say this option is “Out of The Money (OTM)” and has no intrinsic value (IV=$0).

Given this, your counterparty won’t exercise the option. The only impact on your P/L is the $2 premium your counterparty paid you. P/L = $2 (per share).

When S=$28.5

Section titled “When S=$28.5”View the answer to the following problem to see how to calculate the P/L for a Short K=$28 Call @ $2 when S=$28.5

✏️ You have Sold/Written a K=$28 Call. It is about to expire. Suppose S=$28.50 and Premium=$2.

- Will this option be exercised?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- In The Money, so WILL be exercised.

- P/L = $1.50.

Full Explanation:

You have sold an option that obligates you to sell shares of stock worth S=$28.50 for only K=$28 if requested.

You can think of yourself as being matched with a “counterparty” who purchased the option you wrote/sold. Just as you have a Short Call, they have a Long Call. They decide whether to exercise the Long Call they purchased. If they do, you must sell them 100 shares of the underlying stock for K=$28.

By purchasing your shares worth $28.50 for only $28 (a discount of $0.50), your counterparty can make $0.50 per share. Therefore, we say the option is “In The Money (ITM)” and has an Intrinsic Value of $0.50 for its owner.

We’ll assume your counterparty will exercise the option. They will “Call” for your shares to purchase them for K=$28. This will cause a loss for you of $0.50. For example, if you own the shares, you will have to sell them for $0.50 less than you could get on the open market. Alternatively, if you don’t have the shares, you’ll have to buy them for $28.50 and sell them for $0.50 less. Either way, you are $0.50 poorer than you would be if your counterparty hadn't exercised the option. (Correspondingly, they are $0.50 richer. The IV of the option is both your loss and their gain.)

Offsetting the $0.50 loss from selling the shares, you also received a premium of $2. Your final per-share premium is P/L = $2 - $0.50 = $1.50.

(For comparison, your counterparty's final P/L is -$1.50. As always, one party's gain is the other party's loss.)

When S=$29

Section titled “When S=$29”View the answer to the following problem to see how to calculate the P/L for a Short K=$28 Call @ $2 when S=$29

✏️ You have Sold/Written a K=$28 Call. It is about to expire. Suppose S=$29 and Premium=$2.

- Will this option be exercised?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- In The Money, so WILL be exercised.

- P/L = $1.

Full Explanation:

You have sold an option that obligates you to sell shares of stock worth S=$29 for only K=$28 if requested.

You can think of yourself as being matched with a “counterparty” who purchased the option you wrote/sold. Just as you have a Short Call, they have a Long Call. They decide whether to exercise the Long Call they purchased. If they do, you must sell them 100 shares of the underlying stock for K=$28.

By purchasing your shares worth $29 for only $28 (a discount of $1), your counterparty can make $1 per share. Therefore, we say the option is “In The Money (ITM)” and has an Intrinsic Value of $1 for its owner.

We’ll assume your counterparty will exercise the option. They will “Call” for your shares to purchase them for K=$28. This will cause a loss for you of $1. For example, if you own the shares, you will have to sell them for $1 less than you could get on the open market. Alternatively, if you don’t have the shares, you’ll have to buy them for $29 and sell them for $1 less. Either way, you are $1 poorer than you would be if your counterparty hadn't exercised the option. (Correspondingly, they are $1 richer. The IV of the option is both your loss and their gain.)

Offsetting the $1 loss from selling the shares, you also received a premium of $2. Your final per-share premium is P/L = $2 - $1 = $1.

(For comparison, your counterparty's final P/L is -$1. As always, one party's gain is the other party's loss.)

When S=$30

Section titled “When S=$30”View the answer to the following problem to see how to calculate the P/L for a Short K=$28 Call @ $2 when S=$30

✏️ You have Sold/Written a K=$28 Call. It is about to expire. Suppose S=$30 and Premium=$2.

- Will this option be exercised?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- In The Money, so WILL be exercised.

- P/L = -$0.

Full Explanation:

You have sold an option that obligates you to sell shares of stock worth S=$30 for only K=$28 if requested.

You can think of yourself as being matched with a “counterparty” who purchased the option you wrote/sold. Just as you have a Short Call, they have a Long Call. They decide whether to exercise the Long Call they purchased. If they do, you must sell them 100 shares of the underlying stock for K=$28.

By purchasing your shares worth $30 for only $28 (a discount of $2), your counterparty can make $2 per share. Therefore, we say the option is “In The Money (ITM)” and has an Intrinsic Value of $2 for its owner.

We’ll assume your counterparty will exercise the option. They will “Call” for your shares to purchase them for K=$28. This will cause a loss for you of $2. For example, if you own the shares, you will have to sell them for $2 less than you could get on the open market. Alternatively, if you don’t have the shares, you’ll have to buy them for $30 and sell them for $2 less. Either way, you are $2 poorer than you would be if your counterparty hadn't exercised the option. (Correspondingly, they are $2 richer. The IV of the option is both your loss and their gain.)

Offsetting the $2 loss from selling the shares, you also received a premium of $2. Your final per-share premium is P/L = $2 - $2 = -$0.

(For comparison, your counterparty's final P/L is $0. As always, one party's gain is the other party's loss.)

When S=$32

Section titled “When S=$32”View the answer to the following problem to see how to calculate the P/L for a Short K=$28 Call @ $2 when S=$32

✏️ You have Sold/Written a K=$28 Call. It is about to expire. Suppose S=$32 and Premium=$2.

- Will this option be exercised?

- What is your Per-Share Profit or Loss (P/L)?

✔ Click here to view answer

Short Answer:

- In The Money, so WILL be exercised.

- P/L = -$2.

Full Explanation:

You have sold an option that obligates you to sell shares of stock worth S=$32 for only K=$28 if requested.

You can think of yourself as being matched with a “counterparty” who purchased the option you wrote/sold. Just as you have a Short Call, they have a Long Call. They decide whether to exercise the Long Call they purchased. If they do, you must sell them 100 shares of the underlying stock for K=$28.

By purchasing your shares worth $32 for only $28 (a discount of $4), your counterparty can make $4 per share. Therefore, we say the option is “In The Money (ITM)” and has an Intrinsic Value of $4 for its owner.

We’ll assume your counterparty will exercise the option. They will “Call” for your shares to purchase them for K=$28. This will cause a loss for you of $4. For example, if you own the shares, you will have to sell them for $4 less than you could get on the open market. Alternatively, if you don’t have the shares, you’ll have to buy them for $32 and sell them for $4 less. Either way, you are $4 poorer than you would be if your counterparty hadn't exercised the option. (Correspondingly, they are $4 richer. The IV of the option is both your loss and their gain.)

Offsetting the $4 loss from selling the shares, you also received a premium of $2. Your final per-share premium is P/L = $2 - $4 = -$2.

(For comparison, your counterparty's final P/L is $2. As always, one party's gain is the other party's loss.)

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.