🙋 Student Q&A (Lecture 6)

Click here to learn about timestamps and my process for answering questions. Section agendas can be found here. Email office hour questions to rob.mgmte2000@gmail.com. PS1Q2=“Question 2 of Problem Set 1”

📅 Questions covered Saturday, Mar 7

Section titled “📅 Questions covered , Mar 7”🕣

❔ Compounded monthly.

✔ Suppose that you go to a bank and you get a 8% interest rate, compounded monthly. Suppose you deposit $10,000 and earn this rate. What that means is that because there are 12 months in a year, you are paid 8%/12 every month.

After 1 year, you compound once for every month - ie 12 times.

FV = $10,000 × (1+8%/12)^12

Semiannual compounding 8%/2 FV = $10,000 × (1+8%/2)^2

🕣 5:14pm

❔ How is the discount rate also the opportunity cost?

“It measures how much I give up by having to wait a certain amount of time.”

✔

🕣 not covered in video

❔ Excel vs Google Sheets?

✔ For this class, Google Sheets is just as powerful and is free.

🕣 not covered in video

❔ If it doesn’t state monthly vs annual compounding what should we assume?

✔ Generally assume annual.

🕣 not covered in video

❔ Is there a formula in Excel to calculate the IRR for an infinite stream of payments?

✔ No, there isn’t one because Excel assumes that you know the underlying finance, and I guess it just wants you to put the actual formula in. Bruce teaches you the formula that you need in the lecture, so if you just do the formula from the slides, you’re good.

To calculate IRR, always set PV Inflows = PV Outflows For an IRR: Price = Outflows Pmt/i = PV of Inflows PV Inflows = PV Outflows Pmt/i = Price Switcheroo → i = Pmt/Price. This is the formula that you’ll find online if you look up the rate of return on a perpetuity, but we can figure it out ourselves because we understand where the IRR comes from.

🕣 3:50pm

❔ Perpetuities - how does the math work?

✔

📅 Questions covered Sunday, Mar 8 ✅

Section titled “📅 Questions covered Sunday, Mar 8 ✅”🕣 Wrapped up at 2:47pm

❔ Could we do some more IRR questions?

✔ In video

🕣

❔ 1. In your formula excel, you provided an example of various compounding period

- annual where N = 1

- Monthly where N = 12

- Quarterly where N = 4.

Now in the above example, if we are given an annual intrest rate i, for example 10 %, it is my intrepretation that the following will need to be done. Am I on the right track

- If annual , i = 10

- If monthly, i = 10/12

- If quarterly , i = 10/4

✔ Yes. If the annual interest rate is x, and you compound monthly, then you get x/12 every month.

The FV = PV*(1+i/12)^(N*12) N=number of years.

📅 Questions covered Tuesday, Mar 10

Section titled “📅 Questions covered , Mar 10”🕣 7:48pm ish

❔ In the Midterm practice questions, why didn’t we have to keep R+E of the reserves when we lent the money out?

✔

🕣 7:54pm

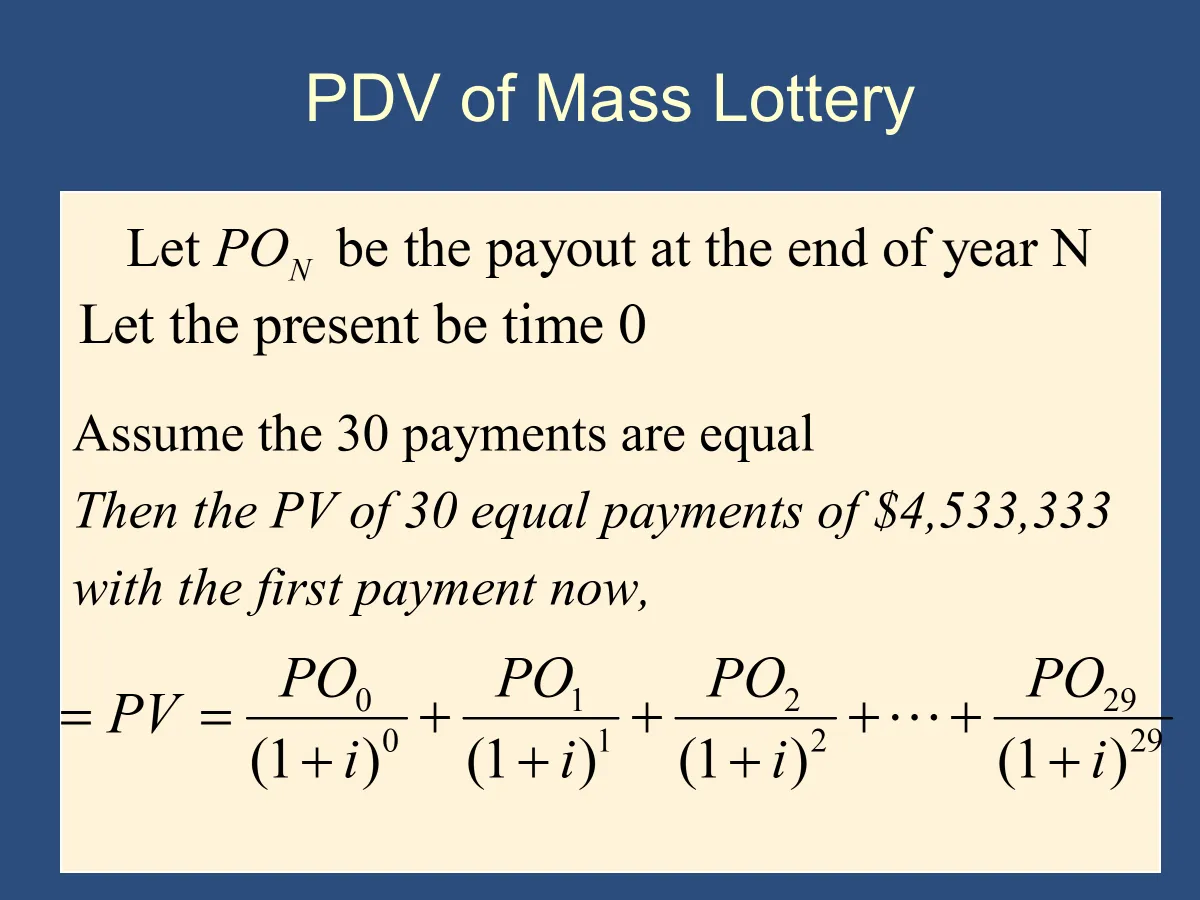

❔ Calculate PV of a stream of payments when you receive the same amount each year.

✔ I’ve shown you Excel, but everything that you’re actually going to be doing on the exam and that you’ll actually get points on doesn’t have anything to do with Excel’s built-in formulas. As I’ve said many times before, the built-in formulas in Excel like =NPV() and =IRR() are only for checking your work.

Suppose you receive $100 every year for the next 5 years. Assume your discount rate is 7%.

PV = $100/(1+7%)^1 +$100/(1+7%)^2 +$100/(1+7%)^3 +$100/(1+7%)^4 +$100/(1+7%)^5

PV = 100/1.07^1 + 100/1.07^2 + 100/1.07^3 + 100/1.07^4 + 100/1.07^5 = $410.02

🕣 8:05pm

❔ If we had to do the following calculation, how should we do it?

✔ You wouldn’t have to do this on an exam because Bruce is much nicer than that. He knows that he can test whether you get the core concepts using simpler examples and he doesn’t think that typing that many numbers into your calculator is that important.

🕣

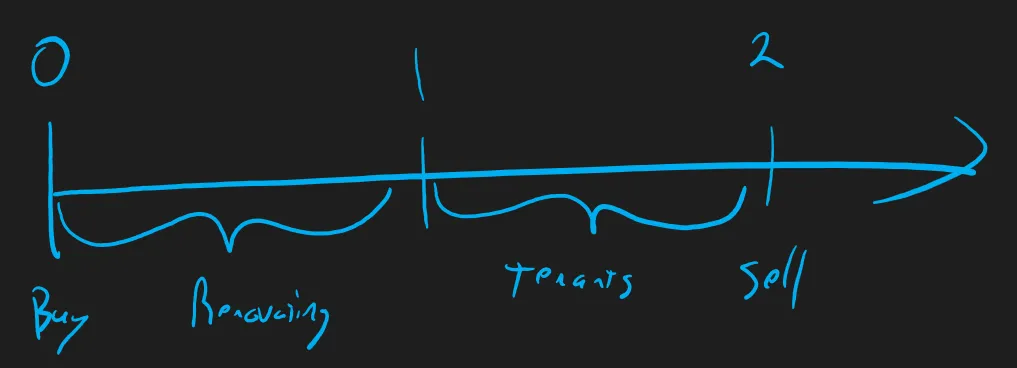

❔Does it matter whether the payment is received at the beginning of the year or the end of the year?

✏️ Suppose that you start a real estate project today. You purchase a run-down property and will renovate it and rent it starting exactly 1 year from now. You will rent it for one year and then will sell it. What is the present value of your rental income, assuming that your tenants prepay for the entire year they will be staying there. In other words, they pay the entire rent on the day they move in (which is the day the renovations are complete, 1 year from now.) The rental income will be $20,000 per year. Your discount rate is 9.7%

✏️ In the above example, the tenants prepaid for the entire year on their move-in day. This is not realistic. Instead, assume that the rent isn’t collected until the end of the year. Redo the problem assuming that the entire rent payment is collected on the day they move out. (We will more typically assume this.) PV = 20000/1.097^2 = $16,619.45

Clearly, timing matters a lot. We call this the time value of money.

🕣 8:26pm

❔ How do you refer to payments easily.

✔ Inflow, outflows.

Net Cashflows = Inflows - Outflows.

If you have inflows of $100 and outflows of $40, then your net cash flows are $60.

If you have inflows of $40 and outflows of $100, then your net cash flows are -$60.

🕣

❔ If you receive 5 payments of $180K a year, with the first payment received in 1 year, what is the NPV if your discount rate is 7%?

✔ PV = 180/1.07^1 + 180/1.07^2 + 180/1.07^3 + 180/1.07^4 + 180/1.07^5 = $738,035

🙋♀️ NPV is the difference between the cash inflows and the cash outflows.

🕣 8:00pm

❔ What is the difference between the perpetuity formula and the regular formula?

✔ Suppose that i=8% If you get $100 once, in one year the formula is:

If you get $100 every year, starting one year from now, and the payments go on forever, you use the perpetuity formula:

🕣 8:45pm

❔What do you do if there are multiple ways to decide if you take on a project? (i.e., what do you do if you can use both the IRR and the NPV rule?)

✔ Either is fine

🕣 8:47pm

❔ What do we do if we have to do the guess and check method because we can’t do it with Algebra?

✔ https://2000.robmunger.com/l6/noalgebra/

🕣 8:55pm

❔ What formula can I use for calculating the PV of something with monthly compounding.

✔

✏️ If I receive $1000 in two years, what is its PV with monthly compounding and an interest rate of 9%?

✔ PV = $1000/(1+9%/12)^(2*12) The general formula is: PV = FV / (1+i/n)^(n*t) n = the number of compounding periods in a year (months: n=12) t = the number of years.

🕣 8:59pm

❔ What formula can I use for calculating the FV of something with monthly compounding.

✔ You do the same idea for FV.

✏️ If I have $1000, what is its PV in two years with monthly compounding and an interest rate of 9%?

✔ FV = (1+9%/12)^(2*12) The general formula is: FV = PV×(1+i/n)^(n*t) n = the number of compounding periods in a year (months: n=12) t = the number of years.

🕣 9:03

❔ Analyzing using FV vs analyzing using PV.

✔ You can always compare multiple projects at any specific point in time. You can compare them at the present by taking the PV of all cash flows. You can also take it in the future, by taking the FV of all cash flows appropriately. The FV numbers will always be larger. Specifically, the FV numbers will be the FV of the PV numbers.

📅 Questions covered Wednesday, Mar 11 ✅

Section titled “📅 Questions covered Wednesday, Mar 11 ✅”🕣 7:47pm

❔ If we understand the questions from the problem sets and the and can do those, do I expect that we’ll do well on the exam?

✔ Yes, I think so! I think that is the most important thing. We’ve had a good group coming to Section, and for those people they have a great understanding of the foundations of the applications of all of these ideas. All you need to do is kind of tie it up with a bow by focusing on the actual problem sets. A lot of what you want to be focusing on now to wrap things up is to make sure that you can apply this within the context of practice problems. Of course, because everything goes back to the slides, make sure that you’re on top of all of the material in the slides.

In terms of the quantitative problems, which are super important, I put down a number of helpful things to practice with on the following page. Make sure that you’ve done these. I think you’d find it really helpful: https://2000.robmunger.com/exam/mtpractice/

As I mentioned, reviewing the slides is also extraordinarily helpful. I can tell from the following questions this person has been reviewing the slides, because it’s the type of question that you start thinking about when you have been reviewing the slides. You start thinking big picture and you start drawing connections.

🕣 7:50pm

❔ When do we use the market for reserves vs the market for money?

✔ This is a natural thing to start thinking about as you are reviewing the slides. You’ll start to notice that we have two separate graphs that we use for determining the interest rate. In lecture four, we use the graph for the supply and demand for money, and then in lecture five we use the supply and demand for reserves. When should you use which?

To some degree, these show up because of the way that the course has evolved. Classically, economists have thought about interest rates as being determined by the supply and demand for money, because the interest rate is how much you pay if you want to borrow money. It is the price of borrowing money. That’s more the big picture perspective, and it’s helpful when we’re thinking about changing the supply of money.

Now, changing the supply of money is what happens when you are in a limited reserves regime. Overall, you should be using the supply and demand for money diagram when you are in a limited reserves regime, like the model that we studied when we were in lecture four.

In contrast, in Lecture 5 we were looking at the ample reserves regime. We’re focusing more on that, and in that context the Fed is more directly setting the federal funds rate. The federal funds rate is, of course, the rate that banks lend reserves to each other, so for that we do what the Fed does, which is we look specifically at the market for reserves. Of course, the Fed doesn’t set the fed funds rate directly; instead, it just sets the discount rate and the interest on reserve balances rate.

Summary:

- We typically use supply and demand for Money when we are analyzing a limited reserves regime. In a limited reserves regime, monetary policy is primarily done by OMOs, which change the supply of money.

- In contrast, in an ample reserves regime, the Fed doesn’t have as much control over the supply of money. Therefore, it operates more directly in the market for reserves, leading us to look at the supply and demand of reserves.

(see video)

https://2000.robmunger.com/l4/4outline/

📅 Questions covered Saturday, Mar 21 ✅

Section titled “📅 Questions covered , Mar 21 ✅”No questions emailed.

📅 No Section on Tuesday, Mar 24

Section titled “📅 No Section on , Mar 24”No section today. For more information, see the announcement on Canvas.

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.