✏️ Arbitrage

Remember that in order to get a high return going forward, you want to buy things cheaply. To understand this, think of a security as something that promises us certain future cash flows.

- If the price of the security is low, then we will get those future cash flows cheaply and will have a high return.

- If the price of a security is high, then we will pay dearly for those future cash flows and we will have a low return.

Therefore, anything that raises the price of a security lowers its future return.

This can be unintuitive, because we think of ourselves as owners of the security, not prospective purchasers. If we own a security already, then we are prospective seller, so naturally we may want a higher price. However, if we don’t own the security yet and we take the future cash flows as given (which we do), then we have a higher return when the price goes down.

Why prices of securities will gravitate towards a fair risk-adjusted return.

Section titled “Why prices of securities will gravitate towards a fair risk-adjusted return.”High risk-adjusted return

Section titled “High risk-adjusted return”Suppose a given security will have a risk-adjusted return that is higher than a typical level.

How would investors (called arbitrageurs) react? Would they buy or sell?

They’d buy! They’d do this because they want to earn a higher risk-adjusted return!

What happens to the price of the security when they buy?

It rises!

When the price of the security rises, then the forward rate of return falls, as we found earlier.

In other words, when the risk-adjusted return of the security is higher than the fair level, that risk-adjusted return will fall because the price of the security will rise. This will keep on happening until the risk-adjusted return of the security matches the risk-adjusted returns of all of the other securities and it’s no longer such a good find.

This is the core idea of the EMH!

The risk adjusted return of the security will fall until it exactly equals the “fair” risk adjusted return.

Low risk-adjusted return

Section titled “Low risk-adjusted return”Suppose a given security will have a risk-adjusted return that is lower than a typical level.

How would investors (called arbitrageurs) react? Would they buy or sell?

They’d sell! They’d do this because they want to avoid a lower return!

What happens to the price of the security when they buy?

It falls!

When the price of the security falls, then the forward rate of return rises, as we found earlier.

In other words, when the risk-adjusted return of the security is lower than the fair level, that risk-adjusted return will rise because the price of the security will fall when people sell it. This will keep on happening until the risk-adjusted return of the security matches the risk-adjusted returns of all of the other securities and it’s no longer such a bad investment.

This is the core idea of the EMH!

The risk adjusted return of the security will rise until it exactly equals the “fair” risk adjusted return.

Summary

Section titled “Summary”Whenever a security has a risk adjusted return that is higher or lower than the fair level, then the return will rise or fall until it exactly matches the fair level.

What is the fair level?

Section titled “What is the fair level?”Suppose I have two stocks, A and B.

We expect that Stock A will, on average, be worth $10 in exactly one year. However, we don’t know what Stock A will actually be worth. Yep, it could be worth much more or it could be worth much less. We don’t know. All that we know is that we expect it to be worth $10 on average. We write this by saying that the expected value of the price of stock A, is $10. We write this as: Let’s assume that it doesn’t pay any dividends.

How much is this stock worth today? . Well, it seems very risky, so we should use a higher discount rate when calculating it’s PDV. Suppose that similarly risky stocks have a 20% return. Then we could apply a 20% discount value to stock A:

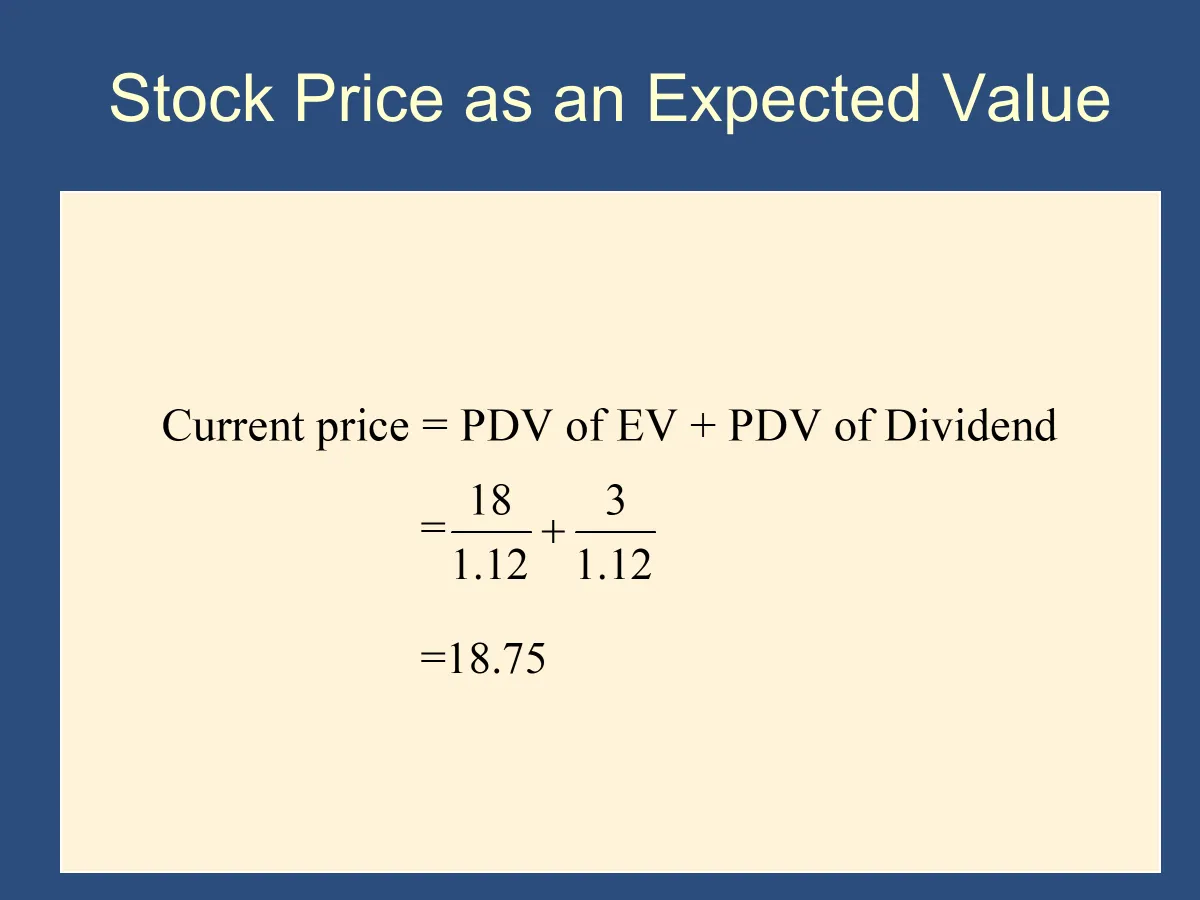

Next, let’s consider Stock B, which is more predictable. Because it’s more predictable, it’s risk characteristics are more attractive, so investors will only demand a return of 15% to hold it.

On average, we only expect it to be worth $8 in the future, but we do expect it to pay a $2 dividend, for sure, in one year. Thus, if you own it, you expect to have a value of $10 in exactly one year. Applying our discount rate, we get:

The above prices are the “fair,” risk adjusted prices for each of the stocks. If you buy stock A for $8.33 and you hold it for a year and sell it for $10, you’ll realize a return of 20% to compensate you for the risk you took on. If you buy stock B for $8.70 and hold it for a year, selling it for $8 and pocketing the $2 dividend, you’ll realize a return of 15% to compensate you for your investment and the risk.

In summary, to calculate the fair value of the stock, you calculate the expected value of the future price of the stock and add any dividends to that. Then you take the present value based on an appropriate discount rate.

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.