🙋 Final Exam StudentQs

Click here to learn about timestamps and my process for answering questions. Section agendas can be found here. Email office hour questions to rob.mgmte2000@gmail.com. PS1Q2=“Question 2 of Problem Set 1” Please read this announcement regarding the section and review session schedule here

📅 Questions covered Saturday, May 9

Section titled “📅 Questions covered , May 9”No questions emailed.

📅 Questions covered Tuesday, May 12

Section titled “📅 Questions covered , May 12”🕣 7:48pm

❔ What does it mean that β=0? β=1? Other values?

There was a question - I don’t know if it will be on the exam.

✔ β = 0 if

- you are talking about the dollar value of a dollar bill. (Because it doesn’t change → it has no volatility → σ = 0 → β=0).

- if you randomly flip coins and get paid based on heads or tails. This is completely random, so it isn’t correlated with the market portfolio at all.

- if you are looking at the risk free rate. The risk free rate doesn’t vary because it is risk free. (Because it doesn’t change → it has no volatility → σ = 0 → β=0).

If β=0, then the expected return of the security (or the portfolio) is r_F according to the CAPM:

β = 1 for

- the market as a whole.

- a portfolio that matches the market as a whole (it has all of the same securities in all of the same proportions - An example would be a perfect index fund that holds close to all the securities in the market, with the holdings roughly proportional to their representation in the actual market)

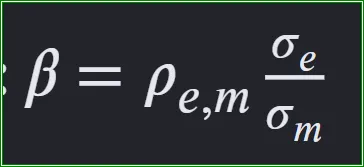

- Based on the formula below, you can see that Beta will have this value if the security (or portfolio) happens to match the market as a whole: the correlation and standard deviation will be the same, so you put the same numbers in and get the same number out. As long as the security has roughly the same volatility and roughly the same correlation as the market, you will get a Beta of 1. Even if it has higher volatility, you can still get a Beta of 1 if that is compensated by a slightly lower correlation. In other words, you could have lots and lots of portfolios and securities with a Beta of 1.

If β=1, then the expected return of the security (or the portfolio) is E[r_M] according to the CAPM:

Based on the formula,

You can see:

- As β increases, you can expect a higher return.

- As β decreases, you can expect a lower return.

- If β is positive (as it almost always is), your expected return will be higher than the risk-free rate.

- If β is negative, your return will be less than the risk-free rate.

Not responsible. (but very helpful)

🕣 8:09pm

❔ Could there be anything on how Fed can raise and lower interest rates? Is that worth covering?

✔ Anything he covered in class is fair game on the exam. He spent a lot of time on this, so he clearly thinks it’s important, and you should review it almost as thoroughly as you did for the midterm.

You can expect something on monod on the final. My guess is military policy will show up on the final, not the midterm. The whole money and banking topic was four weeks, and two of those weeks were focused specifically on the Fed.

Limited reserves regime: (a nice overview) https://prezi.com/view/AzqChnbTFeaAMICMVMWW/

Ample reservers regime: (also see slides and video recording from today) https://2000.robmunger.com/l4/amplereservesfaq/

🕣 8:32pm

❔ If we have to find the value at which there will be a margin call, when will that value be negative versus positive?

✔ You get a margin call when you lose money. The question is: what future contract values will cause you to lose money?

When you buy a future, you’re betting the price will go up, so you’ll lose money if the price goes down. If the price goes down far enough, you might get a margin call. To figure out how far it has to go down to trigger the margin call, you need to do the algebra. Let me know in the chat room or elsewhere if you want that.

If you’re buying a future, you’ll get a margin call if the price goes down far enough. If you’re selling a future, you’re betting the price will fall, which is a little like selling a stock short. If the price rises, you’ll start losing money, and if you lose enough, you’ll get a margin call.

To find the exact number, see this: https://2000.robmunger.com/l13/margins/#:~:text=How%20low%20would%20the%20contract%20price%20have%20to%20fall%20for%20you%20to%20get%20a%20margin%20call%3F

🕣 8:39pm

❔ Practice questions? I already know the problem sets!

✔ https://2000.robmunger.com/exam/mtpractice/ https://2000.robmunger.com/exam/fepractice/ https://2000.robmunger.com/exam/optionspractice

🕣 8:41pm

❔ What resources are fair game during the exam?

✔ https://canvas.harvard.edu/courses/166579/discussion_topics/1292803

- The exam is open book and open notes. This implies that paper or electronic notes (including my website), slides, problem sets, textbooks, spreadsheets, and calculators are all perfectly fine. As long as your work is your own and you don’t have unfair access to test materials, you are within the spirit of our policies. Interactive help from other people, cheat sites, or access to exact questions on the exam are not allowed. Please remember that your screen and webcam are being recorded.

No chatbots or other LLMs like ChatGPT, Claude, Gemini, Deepseek, etc. No search engines like Google Bing, or DuckDuckGo.

🕣 8:47pm

❔ Extra credit? 4th grad paper.

✔ He doesn’t offer that. What he likes to do is handle all the grading and put it in the syllabus.

The fourth upload slot is only there in case you missed a deadline for one of the existing graded papers, and you don’t get any extra credit for submitting the fourth one.

You can submit one (and only one) late graduate paper here. See below for details. You can submit your single late paper here.

🕣 8:49pm

❔ How do we solve for a market rate of return?

✔

✏️ Suppose that the beta for a specific stock is 1.2. If your analysts predict an expected return for this stock of 14% and TBills are earning 4%, what is the expected return on the market implied by this scenario?

✔ We are going to use an approach called plug and chug. We’re going to find an equation that relates what we want to know to what we already know, plug in the numbers, and then chug away with some algebra.

Find equation: Plug In: Chug: ErM = 12.3%

✏️ What is the market risk premium implied by the above scenario?

✔ Market risk premium = Expected return of the market = expected return of the market portfolio = Market risk premium =

📅 Questions covered Wednesday, May 13

Section titled “📅 Questions covered Wednesday, May 13”No questions emailed yet…

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.