🔎 Why does volatility increase the premium of an option?

Bruce argues that stock price volatility increases the premium of an option by providing two examples. The first example is for a call and the second is for a put.

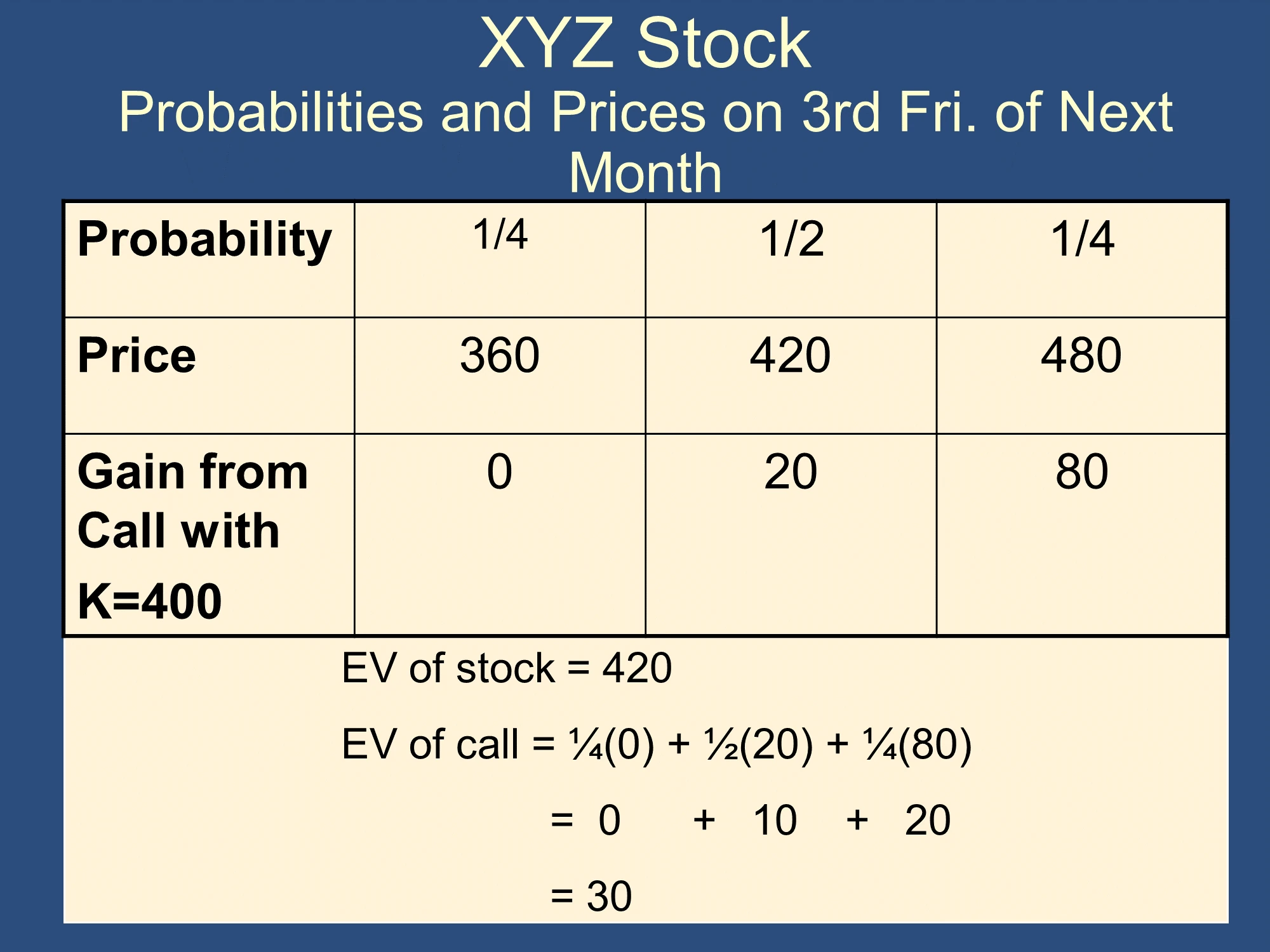

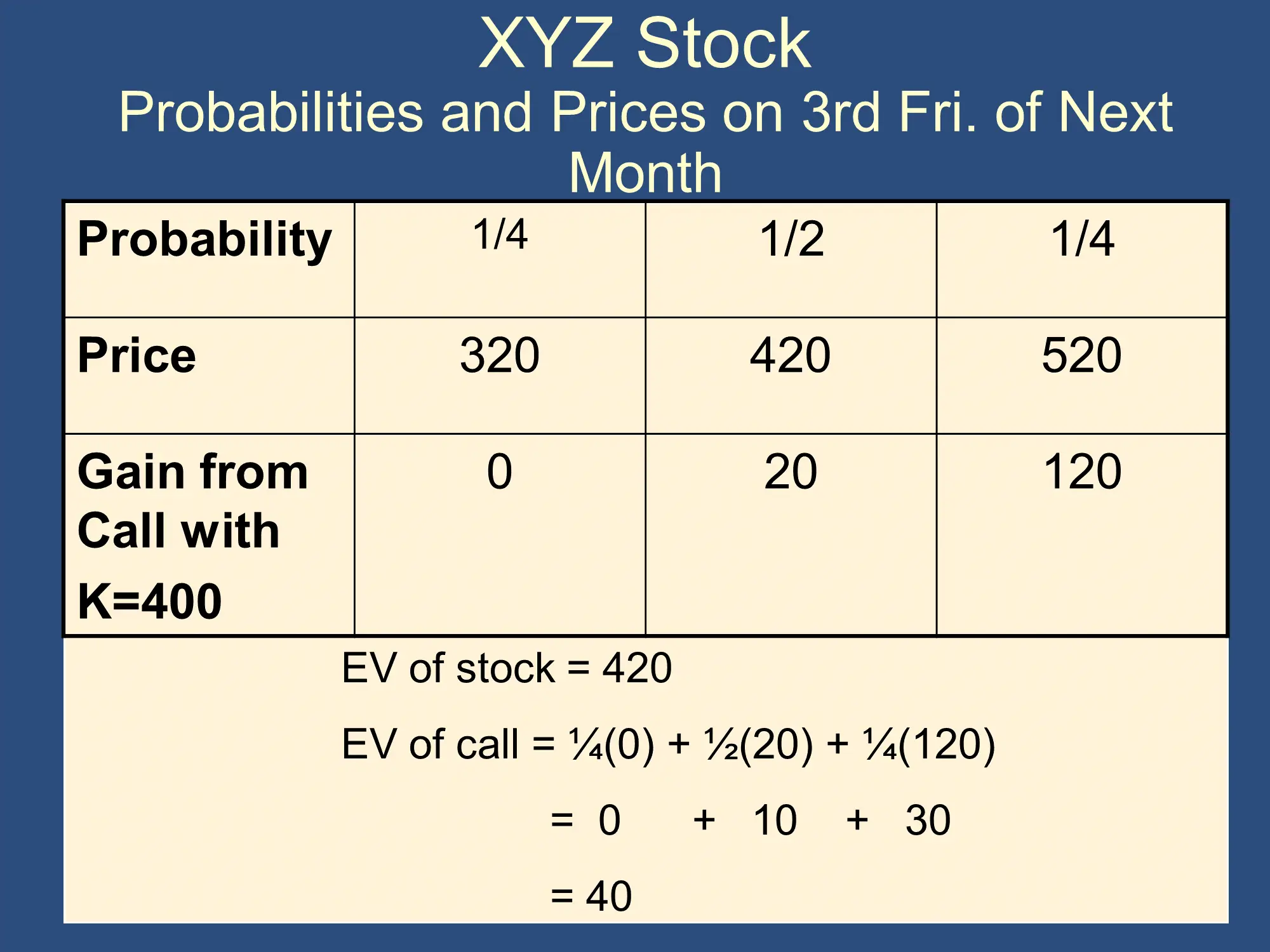

When the stock is volatile/risky the Call option has a higher premium

Section titled “When the stock is volatile/risky the Call option has a higher premium”Call with Low volatility:  The maximum gain is $80. | Call with High volatility:  The maximum gain is $120. |

We see above that with a high volatility stock, the maximal gain is higher. Specifically, the maximal gain is $120 instead of $80. However, the worst gain is still only $0 because if the stock price goes down below $400, you won’t exercise the option. Therefore, the high volatility call is objectively worth more money.

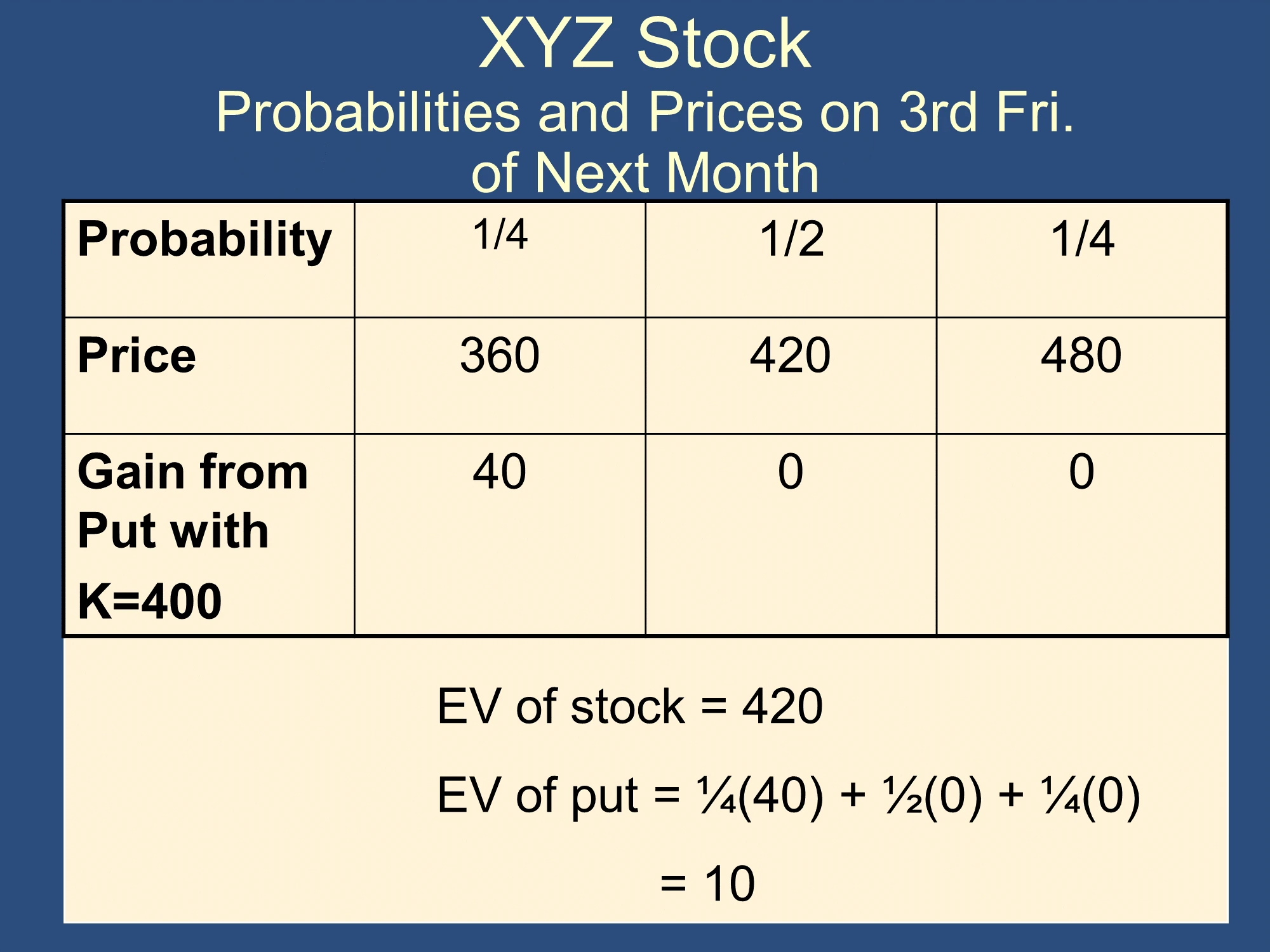

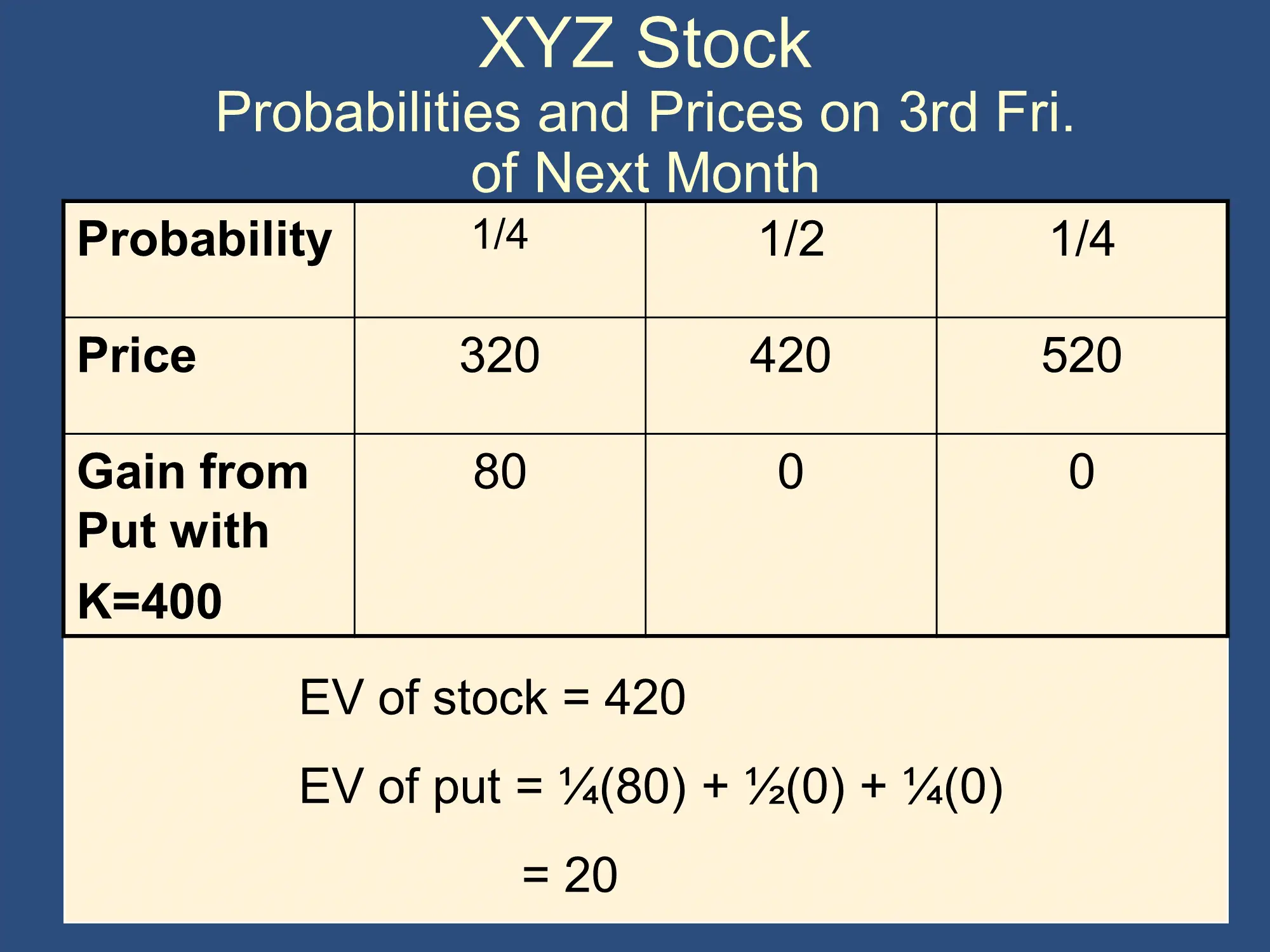

When the stock is volatile/risky the Put option has a higher premium

Section titled “When the stock is volatile/risky the Put option has a higher premium”Put with Low volatility:  Premium comes out to only be $10 | Put with High volatility:  Premium comes out to be $20! |

Once again, we see above that with a high volatility stock, the maximal gain is higher. Specifically, the maximal gain is $80 instead of $40. However, the worst gain is still only $0 because if the stock price goes above $400, you won’t exercise the option. Therefore, the high volatility put is objectively worth more money.

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.