Click here to learn about timestamps and my process for answering questions. Section agendas can be found here. Email office hour questions to rob.mgmte2000@gmail.com. PS1Q2=“Question 2 of Problem Set 1”

📅 Questions covered Saturday, Feb 14

Section titled “📅 Questions covered , Feb 14”🕣 3:18pm

❔ How to ask questions during section. can I interrupt with questions?

✔ Absolutely, you are more than welcome to raise your hand, type a question in the chat room, or even just unmute whenever you feel like it. In general, I have a little bit of a sixth sense for when people unmute. I think it’s because, on the grid of faces, things move around, so sometimes if you just unmute, I’ll just say, “Does anyone have any questions?” You can also put something in the chat room, whatever you like. You can put questions in the chat room as public or private questions, and I think people absolutely love hearing questions.

It’s like in a podcast; it’s better when you have multiple hosts, and so obviously you don’t want to be the host, but I think it’s good to hear different voices. It breaks things up; it breaks up the monotony, so that’s terrific. Okay, so questions are great at any time.

🕣 3:19pm

❔ Can we go over adding tables into Canvas? Can we paste in from Excel?

Does the table have to be two columns. I like to label the quantities and that creates a column.

✔ PASTE ISN’T AVAILABLE DURING THE EXAM.

There’s absolutely no format requirement that the table has to be two columns. As long as the grader understands it, you’re good to go.

🕣 3:34pm

❔ If a question doesn’t say “show your work,” do we still have to show our work?

✔ I think that there’s an implicit expectation that you’re always going to show your work in this class. For any given question, he’s gotten very good at sending me the grading rubric in advance, and so if there’s a question where you’re not sure if you need to show your work, let me know. I think it’d be kind of fun to check, and I can probably pull it up during section. It’ll take a little while, so you’ll have to decide if you want to do that or not, but if you’re interested, I’m sure other students would be interested too.

🕣 3:36pm

❔ When a question asks for a description, how long must the answers be?

When he says ‘explain’ or ‘discuss’, what does he really mean? How much do we actually have to write? When do we need to provide examples? Is listing the definitions enough?

✔ Generally, there are specific ideas that Bruce wants to make sure you have in your answers. These are ideas that he feels are part of the correct answer to the question that’s really asked. That means you don’t have to provide information that definitely isn’t required to answer the question, so you definitely don’t have to put lots of extra information in.

Also, I think that you should think a little bit about econo-

This won’t apply to 85% of the students, but there are some students who are extremely conscientious, particularly if you’ve been out in the corporate world for a while. You feel like you need to write everything properly and in a way that represents you professionally. You definitely do want to present yourself professionally in this class, but you don’t have to demonstrate that in your problem sets so much. You want to be practical and clear, but I have seen one student in the 15 years that I’ve been working with Bruce who, because she worked in HR, dotted all the i’s and crossed all the t’s and spent too long during the exam writing everything out perfectly. She met with me after the midterm and said, “I don’t know how I can do this. I ran out of time.” We went over and reviewed her midterm, and it looked like she had written out everything in beautiful sentences and explained everything. It was just more than she actually needed to provide.

Again, I think that 85% of people are going to write no more than they need to, but you’re not trying to get a job with this homework assignment. You’re trying to make sure that you have effectively answered the questions and that, according to the rubric that Bruce gives to Harry, you’ll get full credits. That’s your only criteria.

The rubric is a bit of a term of art. When you grade, you follow a rubric, which says what people get points for, and the rubric may say something like “Must mention the money multiplier.” That’s great. All you have to do at that point is mention the money multiplier; you don’t have to do a complete sentence. You probably should do a moderately complete sentence, but you don’t have to do an essay about the money multiplier. You just have to mention the money multiplier.

Just try to answer the question and think about what might be important to Bruce that Bruce might think are key elements that are required to answer this question. Often you’ll get a chance to see the rubric, because if you get a question wrong, Harry will often put the relevant part of the rubric into the feedback that he gives you. He’ll just paste it in, so you can get a sense of what Bruce is looking for.

Basically, the rubric looks like this: Bruce goes through each of the questions. He puts the correct answer, and because he’s one of those thorough people, he writes out a really nice answer, but you don’t have to put all that stuff, and then he writes the rubric and says, “These are the expectations that we have for the question.” Usually the rubric is like three bullet points long, maybe it’s a little longer, maybe it’s a little bit shorter. Sometimes the rubric just says “all or none.” That’s because Bruce thinks that this is an easy question that you should be able to get all the things. Usually that would be for a calculation question. For example, if it asks you to calculate the money multiplier, it’s not that hard of a calculation if, in the problem description, you’re given the relevant numbers. Then you’re good to go, and he’s not going to feel very generous with the partial credit on that.

The rubric, by the way, is the thing that provides you the partial credit, but for other things he’s going to have maybe a couple of bullet points explaining where you get the partial credit on the question. Again, the bullet points aren’t going to be super wordy, and they’re just going to describe to Harry what he needs to see in the question. Again, Harry’s on your side; he’s going to give you as many points as he can, consistent with the rubric.

Getting to the specific question: When a question asks for a description, how long must the answer be?

Just try to answer the question. Just write down what you think is a pretty good answer to the question, and then think about: Did I say everything that might be included in the rubric? Given that the rubric is probably only 3 to 5 points long, if I probably included everything.

Moving on to the next question: When he says “explain” or “discuss”, what does he really mean? He wants you to explain something. He wants you to explain your thinking. If he says “discuss”, generally he wants you to explain relevant concepts from class, maybe? I can help you. I think “discuss” is something where you should probably ask me in advance what that means. Say, “Hey, I need your help on this,” and I can pull up the rubric and give you some idea of the depth required. That’s a good way that I can help you on that.

I don’t think you ever really need to do examples. I don’t know, let’s see. Listing the definitions, I would say applying the definitions is more of what Bruce is going to be looking for. Remember the thing here is you want to give him what he thinks is important in answering the question, so I don’t think he’s just “quote the definition”. I guess maybe for some questions that’s what he’s asking, and you want to answer the question that he actually asked.

I know from my own experience grading that when I’m grading something, I always go back and say, “What did the question actually ask?” That’s the standard that I hold the student to.

🕣 3:46pm

❔ Is total reserves in the economy the same thing as total deposits.

✔ Actually, this is something that you can figure out yourself; you just want to go back to the slides. If you do go back to the slides, you’ll see that reserves only have one definition in the slides. Reserves are the ones we talked about a lot at length during the last section, because we knew that they would be important this week. Reserves are vault cash plus deposits at the Fed, and they are reserves that a bank holds in case the depositors withdraw their money. Reserves fundamentally show up on the left-hand side of the bank’s balance sheet. Deposits are a liability for the bank, so they’re totally different. The total reserves in the economy is totally different from the total deposits in the economy.

When I look at this question, I think that there’s a student who’s trying to take a shortcut and doesn’t understand the key ideas and needs to understand the key ideas. With the key ideas, that’s how you figure it out. What makes this problem a little bit difficult is that this is the question that says we need to do the slide review. When we do the slide review, that is going to enable the student to answer the question. Without doing the slide review, we can go back and forth about this or this or this, but if you recall, this is in danger of taking a wrong turn at Albuquerque. It is absolutely vitally important that you not stress out about problems or questions until we’ve had a chance to go over and do the first section.

🕣 3:49pm

❔ If I use something from the slides or Rob’s notes, do I need to cite them as a source?

✔ No

🕣 3:49pm

❔ What is the net profit after taxes formula from the slides

✔ So if you want a technical answer to this, net profit after taxes really stands for net income, though different people will use the various formulas in different ways. On a more precise level, people might use different things for net income. For example, for return over assets there’s a number of different formulas that people use for return over assets.

With that said, this is not a financial statement analysis course, and it doesn’t have accounting as a prerequisite, so we’re going to keep it really simple. You don’t need to know any of that stuff. Generally, in any question where he needs you to apply these formulas, where you need net profit over taxes, there’s only going to be one profit-like number in the question, and you just use that. If he happened to give you two and he said anything to signify that one of them was before taxes and the other one was after taxes, then you’d obviously use the one that was after taxes.

The reason I wanted to dwell on that is the idea that there’s a certain level of detail that Bruce wants you to know and a certain level of detail that he doesn’t care about. Just watch that from the slides, and once you get the hang of it, you’ll feel really comfortable, I think, but you can always ask me for questions.

🕣

❔ I was wondering if you could post the slides for this week’s E-2000 lecture.

✔ I don’t post the slides, actually, so I can’t, but you can always email Bruce. I think he’s going to post them around 3:00. I asked him when he wanted me to post the assignments by. I said, “If you give me 24 hours, I can do it whenever you want.” He said 3:00, so that’s what I’m going to post them by.

In terms of the slides, he’s doing that currently. I’d be happy to take it over, but he hasn’t asked me to.

🕣 4:58pm

❔ Stocks and Bonds

What financial metrics drive weather a company decides to issue Bonds vs stocks?

✔ That’s a complicated decision. We covered that in the Corporate Finance course. There’s a well-known result known as the Modigliani-Miller theorem, which helps decide this. Much of it comes down to finding the right level of leverage based on your ability to tolerate risk and the tax benefits of debt, but there are several other things that we discuss in that course as well.

🕣 5:00pm

❔ In the FAQ section for L1, Q2 , you mention “A company’s stock must be worth at least $40M in total to be listed on the New York Stock Exchange.” Will we be going into how a company’s stock valuation is done ?

✔ Absolutely, we’ll do that when we cover equities.

🕣 5:00pm

❔ Can we do a few more problems on calculating R or E from balance sheet?

✔ Covered that earlier. It’s in the recording. There is also a formula that can be helpful in problems like this. You can find it on my formula sheet, and I’ll give you a screenshot.

🕣

❔ I was solving the first problem set and noticed the question concerning table drawing and I know a similar question was brought up during the first lecture. I wanted to confirm whether drawing by hand or interesting at able unto canva using the icons is still acceptable ? And in addition if you could do a few examples during your office hours on getting the money multiplier please . Thank you . Your notes and help so far in the class has been extremely helpful and i really appreciate it.

✔ You are always more than welcome to use any tool in Canva for drawing tables. I illustrated how to do this at the beginning of the section. If Canva allows you to upload a diagram, you are welcome to do that. I would suggest learning the table editor in case it is helpful during an exam. We did some examples with the money multiplier earlier. We can do more examples if requested during the second section, because we still have a whole other section to do.

🕣 5:03pm

❔ For the reserves question (Question 5, part 3c) in Assignment 1, we need to

Draw a balance sheet for BOA, showing all categories, including the amount of reserves the bank must be holding.

Can you please confirm what percentage we need to use for reserve for required v/s excess?

✔ That question is asking for the actual dollar amount of reserves rather than a reserve ratio such as R or E.

🕣 5:04pm

❔ Lecture 3 - Slide 39

When we calculate ROA, is the ‘Total Assets’ the total assets at the beginning of the quarter, for example, before interest is earned on the assets and added back into ‘Total Assets’?

✔ In this class, you won’t have to worry about that. Different analysts will use different conventions when calculating return on assets. The best way to do it usually is to take the average of the total assets the firm had at the beginning of the time period and at the end of the time period, and then use that as the divisor under a numerator, which is equal to the net profit after taxes. You really don’t need to apply that in this class. It really does go beyond the scope.

If you’re trying to use that to use a problem set question, let me know because you don’t need to do that.

The reason that we take the average of the beginning of the time period and the end of the time period is that the income represents the income earned throughout the entire time period. The best way we can approximate the average balance sheet throughout the entire time period and match the time period over which the income represents is by taking the average of the beginning and the end.

🕣

❔ Lecture 3 - Slide 78

Where do the Feds make money to pay the interest to the bank’s reserves?

If banks keeps more in reserves, does it mean that there is less money supply, and less capital for the public to access? What are the implications?

✔ We’ll talk more about Fed finances later on. The Fed, as we’ll see in the very next lecture, ends up buying massive amounts of bonds. It makes interest on those bonds, and therefore typically it has a large profit.

The way that it makes interest on the bonds is something that you’re going to want to pay attention to. The Fed is the only entity in the world that can just demand that U.S. dollars be printed up and delivered to it so it can create new bank reserves out of thin air and use those to buy bonds. It has a massive bond portfolio, the largest in the world, and it gets a lot of income from those. That’s where it gets the money to pay interest on reserves.

🕣 5:07pm

❔ Lecture 3 - Slide 84

The statement, ‘Eventually the bank will need to do (3) and (4)’. Does this mean banks will choose options (3) and (4) before (1) and (2)? And why would that be the case?

Final question, not sure if I answered my own question:

If hypothetically we are interested in calculating the ‘Initial Deposits’ of the entire United States, if we know the value of ‘Total Deposits’ in the United States, how do we go about calculating the Money Multiplier. Does this mean we have to go to each bank to get the Reserve and Excess Reserve number?

✔ Banks will have their own reasons in deciding whether it will choose option one, two, three, or four first, and different banks may make different choices. We don’t know what it will do, but we do know that it can’t do one and two forever, so eventually it will have to choose three or four. That’s all you need to know: that eventually it will choose three or four. The reason that you need to know that is that’s why we know that the reverse money multiplier process will play out.

If you wanted to get the excess reserve ratio, you would literally have to gather data from all the banks. Sometimes data on banks is pretty limited, and this is why. It’s expensive to gather information about the entire financial system in a country.

🕣 5:08pm

❔ Try to do problem set interpretation.

✔ done earlier

🕣

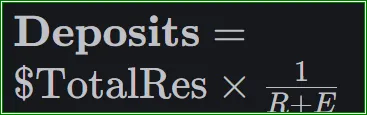

❔ How do reserves in the entire economy relate to deposits in the entire economy?

✔ We can see how reserves in the entire economy relate to deposits in the entire economy by recognizing that reserves and deposits from the entire economy are made up of the reserves and the deposits in individual banks.

For every bank in the economy: Deposits × R = $Required Reserves. Deposits × E = $Excess Reserves Deposits × (R + E) = $Total Reserves

If all banks have the same excess reserve ratio, then you can add up each of these equations for each of the individual banks to get corresponding equations for the entire economy. : Total Deposits in entire economy × R = $Required Reserves in entire economy. Total Deposits in entire economy × E = $Excess Reserves in entire economy. Total Deposits in entire economy × (R+E) = $Total Reserves in entire economy.

Based on the above equation, if you know R+E:

- If you know the total deposits in the entire economy, you can always figure out the total reserves in the entire economy.

- If you know the total reserves in the entire economy, you can always figure out the total deposits in the entire economy.

You can use this key equation for before and after e-changes. You could calculate the total deposits in the entire economy based on an old version of required or excess reserves. Returns required or excess reserve ratios and then calculate it again based on a new version.

🕣 5:16pm

❔ Can you solve the following problem that I made up?

✏️ In the entire economy: Deposits = $50M R=2% E=3% If the if the Federal Reserve decides to reduce the Required reserve ratio by 1 percent and the bank uses all its reserve for loans, what would the balance sheet look like and how would we calculate the new equilibrium? Assume E doesn’t change.

✔ Yes, we can solve this using the equations and the analysis that I discussed in the section immediately above. Let’s plug the above numbers into that equation. Total Deposits in entire economy × (R+E) = $Total Reserves in entire economy. 50M × (2%+3%) = $Total Reserves in entire economy. = 50M × 5% = 2.5M

If the Federal Reserve decreased the R by one percent, then there would be chaos for a while. Eventually, when things settled down and banks were able to make loans with all of the new reserves that they didn’t have to hold, the same equations would still be true. Therefore, we can use the same equation again to find out what the economy would look like after all of the changes. Naturally, when we’re doing this, we have to think about what will stay the same and what will change.

The banks no longer have to hold quite as much of their reserves as they had to hold before, so they will make new deposits. Therefore, we expect the total deposits in the entire economy to rise.

Reserves are an asset owned by the bank. They’re not going to change just because regulations changed. Therefore, we will use the original amount of total reserves, and we will get a new amount of total deposits.

Old Reserves = 2.5M, Old Deposits = 50M, Deposits will change, but reserves stay the same, as described above.

Total Deposits in entire economy × (R+E) = $Total Reserves in entire economy. Total Deposits in entire economy × (1%+3%) = $2.5M Total Deposits in entire economy = $2.5/(1%+3%) = 62.5M

In other words, after everything has shaken out and after the banks are able to make new loans with the money that they no longer have to hold as reserves, and the money multiplier process has played out, the new total deposits in the entire economy will be $62.5 million.

So far, we’ve used this example for figuring out what happens if the required reserves change, but we could also think about what would happen if the total amount of excess reserves that the banks decide to hold changes. Let’s rewrite the question to do that.

✏️ In the entire economy: Deposits = $50M R=2% E=3% If the banks all simultaneously decide to decrease their target excess reserve ratio from 3% to 2%, and then they decide to all use the new reserves that they no longer want to hold as excess reserves and they use these for loans, what will the new equilibrium be?

new equilibirum = how would the balance sheet and the total deposits in the money in the economy change once the money multiplier process is played out?

R hasn’t changed, so we just use the same equation: Total Deposits in entire economy × (2%+2%) = 2.5M Total Deposits in entire economy = 2.5M /(2%+2%) = $62.5 millio

🕣

❔ Money multiplier = 1/(R+E)

What if E and R are both 0?

✔ The only way that R and E could both be zero is if the bank decided to hold zero reserves. Let’s confirm that by looking at our formulas.

📅 Questions covered Tuesday, Feb 17

Section titled “📅 Questions covered , Feb 17”🕣 7:45pm

❔ Could we review how to determine the total reserves in the economy from the total deposits and how to determine the total deposits in the economy from the total reserves?

✔ Earlier, we argued that the following formulas are true for all banks. For every bank in the economy: Deposits × R = $Required Reserves. Deposits × E = $Excess Reserves Deposits × (R + E) = $Total Reserves

Because the above equations apply to all banks, you can add them up if R and E are the same for all banks, and then they will apply for the total amounts in the entire economy. Total Deposits in entire economy × R = $Required Reserves in entire economy. Total Deposits in entire economy × E = $Excess Reserves in entire economy. Total Deposits in entire economy × (R+E) = $Total Reserves in entire economy.

If you divide each equation by Total Deposits in entire economy, you get: R = $Required Reserves in entire economy/ Total Deposits in entire economy E = $Excess Reserves in entire economy / Total Deposits in entire economy (R+E) = $Total Reserves in entire economy / Total Deposits in entire economy

If you divide by the reserve ratios, you get: Total Deposits in entire economy = $Required Reserves in entire economy / R Total Deposits in entire economy = $Excess Reserves in entire economy / E Total Deposits in entire economy = $Total Reserves in entire economy × (1/(R+E))

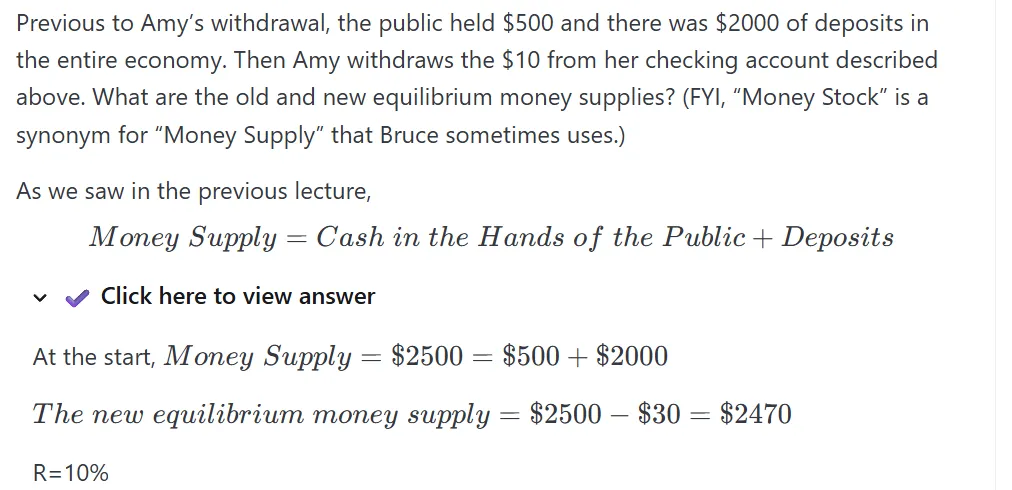

✏️ Suppose that the cash held by the public in an economy is $5 billion. The amount of total reserves is $10 billion. The required reserve ratio is 8%, and the excess reserve ratio is 12%. What is the money supply?

✔

MS = CHP + Deposits (this is the definition of the M1 money supply)

To use this, we need to know deposits. We calculate deposits as

MS = CHP + Deposits Money Stock = $5B + $50B = $55B

🕣

❔ What is the difference between cash held by the public and the change in cash held by the public?

✔ Suppose we’re in a country of one person, and there’s one person in one bank. I’m the person, and I have $100. In this case, the cash held by the public is $100. Suppose that I don’t have anything in my checking account; then deposits in this economy, as it stands, are $0.

If I deposit $100 into my checking account, then the change in cash held by the public will be -$20. The cash held by the public will be $80. The change in cash held by the public will be negative whenever I deposit money. However, if I go back to the bank and I withdraw half of the money that I just deposited, then the new change in cash held by the public will be a positive 10 because I have just withdrawn $10.

So, change in cash held by the public can be a positive or negative number, but in these three situations the total cash held by the public will always be a positive number.

- At first it was $100.

- After I deposited the $20, it became $80.

- Finally, after I withdrew half of the deposited money, the cash held by the public is $90.

🕣 8:07pm

❔ I found two different ways to solve a problem in which a reserve ratio has changed. I’m not sure why I got the same number both times. Could we go over an example?

✔ 🙋♂️ Actually, the previous question answers my question.

🕣 8:12pm

❔ #10 Interpretation - 4c. If the total money stock (supply) is $10B, find the total amount of reserves held by banks in the economy.

Are we supposed to use some of the numbers from above?

If I use the amount of reserves from above, then it’s already given me the answer to the question, so I feel like I can’t use the reserves from above.

✔To answer this question, you do indeed have to use numbers from above. It’s very common in a question in this class that sub-parts of the same problem will build on each other. Typically:

- Problem 3A will build on the introduction to Problem 3.

- Problem 3B will build on 3A and on the introduction.

- Problem 3C will build on 3B, 3A, and the introduction.

All of them will build on anything that you see above them that was just kind of a little interstitial comment that he sometimes adds. Yes, you definitely want to build on the material earlier, and you have to in order to solve this question. Definitely be looking above on the problem set to find helpful context.

🕣 8:18pm

❔ If a question asks for a percentage of checking deposits, do we need to also include the dollar amount?

✔ He’s going to make his expectations clear, so you just want to read the question really carefully. Like I said, when he’s grading these things, he looks at the question. If the question didn’t ask for the dollar amount also, then he’d feel like he’d be a real jerk if he were to put that in the grading rubric. He’s not going to put that in the grading rubric.

The only thing where you have to be really careful is if he says “explain.” You know what counts as an explanation? What’s important to explain? You want to recognize that what’s important to explain is what Bruce thinks is important to explain. How do you know what Bruce thinks is important to explain? Think about what he presented in class. You don’t have to present all of it, like I said. The rubric usually is just a couple bullet points, so the answers can be very concise.

🕣 8:15pm

❔ How do we write a leverage ratio?

✔ Again, language is very flexible. Typically in finance it’s different from a math class. In a math class, you might refer to ratios by doing 7:1 or 7:1. In many financial applications, you would just write that the leverage ratio is seven, but people are still going to understand you if you say 7:1. It makes it very clear that you’re talking about a ratio context.

🕣

❔ This is an intrepretation question on a problem set - 4c. If the total money stock (supply) is $XB, find the total amount of reserves held by banks in the economy. Is the stock just given to confuse us?

✔ Terminology in finance is a pain. People say what they want to, and he just says “money stock” instead of “money supply”, and you just have to roll with it. He’s not trying to confuse you, and I apologize if he does, but I’m here to help.

🕣

❔ 3e - does the total reserves change?

Now suppose that all banks in the economy decide to reduce excess reserves to just 1%.

✔ Banks decide how many reserves they want to hold. Legally, they have to hold a certain amount of required reserves. As we’ve discussed, the dollar amount of required reserves they have to hold is determined by the required reserve ratio and their total amount of deposits, but they may want to hold more than that. You can always hold more than that if you want to. The amount of excess reserve they hold, either as a dollar or as a percentage, is something that they choose. In this question, we’re being told that they have changed their mind. Earlier, they wanted to hold, I think, 3%. I forget; they wanted to hold some larger percent, and then they lowered how many reserves they wanted to hold down to 1%. They have changed their opinion and they have changed their behavior. Reserves consist of two things, as we know:

- They are literal dollar bills in the bank, so that’s vault cash, and that definitely won’t change.

- The other component of reserves, as we know, are deposits at the Fed. These are money that the bank has deposited at the Fed. Now the Fed still owes them that money, so those reserves still exist. Those also won’t change.

The bank could say, “Well, we don’t want those anymore because we don’t want as many excess reserves,” but they’re definitely not going to do that, because that’s that stuff’s equivalent to cash. If they didn’t want that, they would just reserve it and lend the money out. No one’s giving away money, and so total reserves won’t change, because total reserves are valuable. The bank doesn’t want to give those up. They don’t want to give up their dollar bills. They don’t want to give their deposits to the Fed, and they still own the dollar bills and they still own the deposit the Fed has, so that won’t change.

🕣 8:32

❔ What do we use for calculators during the exam? Can we use a calculator on the platform? Can we use a cell phone?

✔ Proctorio provides a calculator for you, so you definitely can use a calculator within the platform. If you want to try out that calculator, you can use the Proctorio readiness quiz. It’s just a basic calculator on screen; you can totally use it.

You can’t use a cell phone. There’s only one device that can be used for communication. You can only use your computer, so you can’t use like an iPad or a cell phone, but you can use a hand-held calculator if you want one. If you hate the Proctorio calculator, you can also use an online calculator. Those are fine too, as long as it’s just a calculator or spreadsheet; those are totally fine.

🕣 8:33pm

❔ On the problem sets and the exams, do we need to show $ or % while solving the problem or is it ok for the final answer to reflect the correct value like 100$, 2M,10%?

✔ I don’t think it’s a big deal if your intermediate calculations don’t include dollar signs. I would include percentage signs for intermediate calculations.

If you omit a dollar sign, then I still know it’s a dollar amount because I can look at the formula and see what you’ve been doing and get that. If you write 20 when you mean 20%, 20 and 20% are pretty different numbers. You probably want to put a percentage sign in.

If you don’t like putting the percentage sign in, 20% is equivalent to .20, so you could just write .20. That would be perfectly legitimate. To be honest, if you did neglect to put the percentage sign in, you’d probably be fine. You’re just giving a little bit less information to the grader, and you’d probably be fine, but it’s not quite as cautious as you probably want to be, so I’d probably put the percentage on.

🕣 8:34pm

❔ 1.In the solution below, I’m not getting where the 30 came from

✔The 30 comes from a previous problem. Like with Bruce’s problem, sometimes in my problems I’ll break it down into subparts, and the later subparts build on the earlier subparts.

🕣 8:35pm

❔ What is the Road Show? One of the students mentioned it and asked a question about it during the 02.10.2026 Section.

✔ When a company wants to do an IPO, it hires an investment bank to help them sell shares to the public. It’s called an initial public offering because it’s the first time that those shares of stock have been offered to the public.

The investment bank will go to various big investors in various cities and present about the stock. They’ll often bring the company’s management with them. This is called a road show. It helps the investment bank and the issuing company to sell all of the shares that they need to sell on the day of the IPO. This ensures that there’s lots of demand for the shares, that the stock price doesn’t plummet soon afterwards, and that they get a good price when they’re selling the shares in the primary market.

🕣

❔ How does crypto impact M1? Lots of people are using various crypto exchanges as both savings and debit accounts. M2?

✔M1 and M2 are precisely defined statistics. They have to be so that the agency that collects the statistics can get a precise number, and so that all the users of the statistic know exactly what it is. Therefore, M1 and M2 are based only on savings deposits and checking deposits at regulated depository institutions over time.

New measures of the money supply may be created to capture crypto, but in general most economists would say that, for money, most money is most useful if its value doesn’t fluctuate. They may be hesitant to add that to a money supply. Who knows what they’ll do? It’s tough to predict the future, and it’s going to be hard because the crypto space is changing so rapidly. None the less, at present, crypto is not accounted for in either M1 or M2.

🕣

❔ Is crypto considered currency? Money?

✔Whether something is considered money or not is very subjective. As we’ve seen, whether something is money or not is a bit of a spectrum. Something is more money-like if it’s used to make payments and if it can easily be converted at a good price to other forms of money. In other words, if it is liquid.

Most would consider crypto because you can buy things with it, but the number of things that you can buy is still relatively limited. I can’t get a Snickers bar at most convenience stores with it at this point. Also, its value can fluctuate, and most people are risk averse and don’t want the value of the money in their wallet changing over time. Usually one of the traits of money is that it should be a good store of value. In crypto, it isn’t very good at all as a store of value. It has a relatively high volatility if you measure its standard deviation.

I guess you just have to say there are aspects of crypto that are money-like and aspects that aren’t money-like.

🕣

❔ Interpretation: 3c. Bank of America (BOA) has $300 million in deposits, $10 million in bank capital (net worth), $203 million in loans, and $80 million in other assets.

Draw a balance sheet for BOA, showing all categories, including the amount of reserves the bank must be holding.

✔

🕣 8:45pm

❔ Do we have to click submit

✔ no

🕣 8:49pm

❔ If there was only one bank, the Money Multiplier feels like a Ponzi scheme. Does it support the idea of increasing returns to scale for banks’ economies of scale, and would that be a reason for bank mergers?

✔ It is quite mysterious. It would be a little bit strange if there was only one bank, but every time that a bank lends money out to a customer, it’s providing a valuable service to that customer. Every time it takes deposits from a customer, it’s providing a valuable service to that customer as well. It’s not like the bank isn’t providing very, very valuable services to the economy. If an economy doesn’t have money or a financial system, it tends to grow very, very slowly. That’s been tested in many, many economies.

Recently I’ve been learning about China. I just went to China, so I’ve been reading about their history. We tend to think that a lot of the trade with China had to do with the rest of the world loving Chinese porcelain and tea, which they did. On the flip side, China didn’t have enough money. When a lot of this trade was going on, it was just when the New World had been discovered and Spain was pulling out massive amounts of gold and silver from the New World. At the same time, China was like, “Yeah, we need this money.” Their economy was being transformed and commercialized during the Ming Empire because of the silver that was coming in. Not everybody was happy with it, but the bottom line is money is important for any economy to function. They’re not just predators; they’re providing valuable financial services.

In some sense, that could be a reason for mergers, but it’s not the circularity of the funding flows that makes it a reason for mergers. It’s just the fact that the more of a merger you have, the more you benefit from economies of scale and scope and diversification.

🕣 8:51pm

❔ Are there other types of time deposits?

✔There are a very wide variety of different types of time deposits. In our system, companies can set up all sorts of financial instruments with different characteristics. Sometimes banks will have fixed interest rates on their time deposits, and some will be tradable. Time deposits made for large companies to store their money short term are often tradable. That’s known as a negotiable certificate of deposit, and that makes these large companies more likely to do certificates of deposit.

There can be various levels of penalties or no penalties if you withdraw your money early. There’s a wide variety of different time deposits in the US and also in other countries. Different time deposits in different countries may have different traits based on cultural facts and what people are used to and what the competitive market dictates.

🕣 8:52pm

❔ Why are money market mutual funds safe? Can you elaborate on that?

How do they always keep the share at one dollar per share?

✔Money market mutual funds tend to be quite safe; they’re definitely not nearly as safe as deposit accounts. A deposit account is insured by the Federal Deposit Insurance Corporation (or by a corresponding institution for credit unions or other types of deposit-taking institutions), so they’re all really, really safe, as places to put your money with another institution. About as safe as it gets, typically. If any of these things were to fail, the government is going to step in in some way. The FDIC is not part of the federal government; it’s a separate institution within the government, but pretty much you’re almost getting to the full faith and credit of the United States government level of safety. Money market mutual funds aren’t like that at all. Money market mutual funds are just a place you give your money to someone, and they say, “Okay, I’m going to invest your money in ways that are very, very safe, so I’m going to work very, very hard to make sure that for every dollar that you give me I can always give you back a dollar. Usually I’ll be able to give you a little bit more because I’m earning a little bit of interest.”

How do the managers of the money market mutual funds do that? Basically, what they do is they invest in the safest instruments that they can, such as United States government treasury bills. We’ll learn all about those when we do bonds, but they are IOUs from the government, and assuming that the government doesn’t default, they are perfectly safe. Also, they’re only IOUs that last for less than a year, so if the government is going to default more than a year from now, you’re still safe. Hopefully the government will never default; it never has, and hopefully it never will, but that’s why they are often considered safe, because the government could default. They’re not perfectly safe. Also, money market mutual funds don’t just invest in these treasury IOUs called T-bills. If a money market mutual fund does invest in these treasury bills only, then it’s known as a treasury money market fund. I had one of those, but now I invest in a prime money market fund, in which the manager of the mutual fund will invest not just in T-bills but will invest in very short IOUs from companies known as commercial paper and other agencies, et cetera. The idea is only investing in very, very safe IOUs, because the repayment scheme is given and because you’re quite confident that you’re actually going to be repaid. They feel confident that they will always be able to keep the value of one dollar per share.

🕣 8:56pm

❔ How can someone create a new bank? What’s that process like?

✔When people say “banks,” they are most frequently referring to what is known as a deposit-taking institution. As I was suggesting above, a deposit-taking institution is not like a mutual fund. You’re really backed up by these pseudo-government entities like the FDIC if you deposit money in a depository institution. If anyone is going to set up a depository institution, the FDIC or a similar institution is going to want to know all about it before they insure them. After all, FDIC is the Federal Depository Insurance Corporation. It’s an insurance company, and just like your insurance company might, if you want to get a new policy, really check into you, the FDIC is going to do the same. You also have to get a charter from a chartering agency within the state or the national government. All of these things: they’re going to be checking your character. They’re going to be checking the quality of your business plan. They’re going to be checking your experience. They’re going to be checking:

- Do you have good product/market fit?

- Is there a need for a bank?

- Do you have funding?

- Do you have enough capital that you’ve raised?

- Enough bank capital?

They’ll check all of these things. There’s a huge amount of paperwork, but that’s what it takes to keep your deposit safe. You don’t have that when you put your money, for example, in crypto. In crypto, it could all go away, as it did with Sam Bankman-Fried; they can just go away, and in crypto they call it “rug pulled.” You can get rug pulled all you want in crypto, but this stuff is really very carefully monitored by various agencies within the government, including the Fed. One of the things that the Federal Reserve does, which we’ll start learning about today or next time when you watch the next lecture, is that it does supervise the banks and make sure that the banks aren’t doing anything risky. If you’re curious about this next Christmas, if you watch It’s a Wonderful Life, you’ll notice that there was a bank examiner coming into the bank, and that precipitated the crisis. It is that the teller, I think, was drunk and lost some money, and the bank examiner said, “We may have to shut you down, perhaps.” That’s an example of how the various levels of government regulate these depository institutions and make it a little bit hard to set up a new bank. You just have to go through all the paperwork and prove that you’re the real deal.

🕣 8:59pm

❔ When and why would we use the debt to equity ratio vs the leverage ratio?

✔When and why would we use the debt-to-equity ratio versus the leverage ratio? They do show you roughly the same thing. In fact, there is a mathematical relationship between them, but the intuition behind them is different.

One is saying how much debt do you have compared to your equity? The other one is saying how many assets do you have compared to your equity? The first one, the debt-to-equity ratio, is a little bit more commonly used and it’s very intuitive, because when you look at the leverage ratio, you’re trying to figure out how much debt they have. Debt is another word for leverage, so it’s very intuitive.

The leverage ratio, which takes assets and divides them by equity, is a little bit harder to interpret, but it can be used for something called DuPont analysis, which we cover in corporate finance in the spring and capital markets and investments in the fall. It helps you break down and understand where the return on equity of a firm comes from, and that, I think, would be the killer app of the leverage ratio.

In some sense, most people will use the debt-to-equity ratio. You use the leverage ratio more if you’re doing DuPont analysis. Otherwise, they’re more or less equivalent, just with slightly different intuitions.

🕣 9:00pm

❔ Is NIM always a percentage?

✔Net interest margin is when you compare the income that you’re getting from your assets to the total amount of assets. Because it’s a ratio, you can easily represent it as a percentage, and that is indeed what is typically done.

Again, finance is about people trying to get things done, so it’s up to them whether they want to do it as a percentage or as a decimal, but percentage is more common.

🕣 9:01pm

❔ Why were the banks giving out so many real estate loans in 2007? It looks like poor risk management.

✔ If you’re ever looking for a paper topic, it is fine to do as your source instead of doing an article. You can also do a good finance movie. Some excellent finance movies include:

- Margin Call

- Too Big to Fail

- Barbarians at the Gate

I don’t see The Big Short, but The Big Short is a great movie that explains some of the problems that led to the banks giving out so many real estate loans in 2007. It was a huge problem; it really damaged the world, the world economy. Historically speaking, when you damage the financial system, you tend to have prolonged unemployment, very damaging unemployment. Normally, we expect the unemployment level in the United States to be hovering above and below 5%. It got up to 10% after the Great Financial Crisis and stayed high for a while. When you have unemployment for that long, you tend to have a lot of populism. Sometimes, you will have the rise of populist politicians like Trump, so it was a big deal; it affected a lot of things, and the question is why do they do it? Economists analyze this through the notion of moral hazard. The problem here is that the banks were lending out loans, and they would sell the loans to someone else who would package it up in something that we’ll learn about later called a mortgage-backed security or collateralized debt obligation. If you want to learn about those in a really fun way with a fun movie, which I think has Brad Pitt in it and many great actors, watch The Big Short. It’s a great movie. Basically, what they were doing is they were packaging up the loans; it was someone else’s problem, so they said, “Well, we’ll sell these on to someone else who really cares.”

🕣 9:04pm

❔ How do we know if a bank is profitable? How exactly do we define profitability on a balance sheet?

✔If Net income>0, ie if ROE and ROA are >0

🕣 9:06pm

❔ What happens when a bank is insolvent?

✔Like I said, banks are very heavily regulated because the FDIC is insuring them. Banks are required by what are known as the Basel accords to always keep a certain amount of bank capital. If that bank capital gets to be less than zero, they’re called insolvent. Before it gets to be less than zero, the regulating authorities in their country will shut the bank down or at least come in and tell them that they can’t do things, they can’t pay dividends, and they have to sell off assets until they can get their bank capital up to a positive amount. They’re constantly being watched, and hopefully before they become insolvent, they will have the regulators step in and take action and fix things and figure out what’s going on in the business and fire the management or whatever it takes.

Of course, regulators can’t always do what they want to do. They have to abide by the rule of law, and that may make things a little bit more difficult, but obviously it’s a good thing to be constrained by the rule of law. If you don’t want your regulators just doing whatever they think is right.

A limitation on this system is that regulators only have so much information. With Silicon Valley Bank, it was actually because it had done the wrong investments, and we will learn later on, right after the midterm, about interest rate risk. It was killed by interest rate risk. It was pretty much dead, but no one knew that it was dead because of some accounting rules. They didn’t have to admit that they were dead, that they were insolvent, even though they were insolvent. At a certain point, they were a little bit low on money, and they had to sell some bonds. When they did that, that kicked off some accounting rules, and all of a sudden everybody knew that they were dead, and then everybody started pulling their money out, and the whole thing collapsed.

I guess the bottom line is sometimes a bank may be insolvent, but if the regulators don’t have the signals to know that it is, they are insolvent, maybe nothing will happen. If you don’t have to sell the bonds and trigger the accounting rule, you may get away with it for a little while. If you’re lucky, maybe you’ll be profitable enough that you’ll be able to increase your bank capital, because one of the things that we talked about is that changes in bank capital come from when you’re profitable. In the examples we did at the beginning of the last section, it was when you were profitable that you boosted up. When a loan defaulted, bank capital went down; when you got interest, bank capital went up. If you can keep on being profitable for a while, you can increase your bank capital and maybe not be insolvent anymore. When you’re in that situation where you’re kind of dead but nobody knows it, that’s sometimes called a zombie bank. They’re not going to be making any loans, because they’re really trying not to die; they’re just trying to survive to the next year.

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.