🙋 Student Q&A (Lecture 12)

This content is not available in your language yet.

Click here to learn about timestamps and my process for answering questions. Section agendas can be found here. Email office hour questions to rob.mgmte2000@gmail.com. PS1Q2=“Question 2 of Problem Set 1”

📅 Questions covered Saturday, May 2

Section titled “📅 Questions covered , May 2”🙋 Sitting with the material and practicing. I think I just need to sit down

🕣 3:20pm

❔ Time management for final exam prep.

✔

🕣 4:21pm

❔ How do you manage a bull spread as time passes?

✔ When you are done with the strategy, you can always close out the strategy by closing out the individual two calls (buy to close and sell to close). If the stock price has moved in the direction you had hoped and if markets are efficient, you will make money (at least before any fees).

🕣 4:24pm

❔ How do we find the premium for a option or strategy?

Can we do a concrete one for a strategy?

✔

If markets are efficient (EMH)…

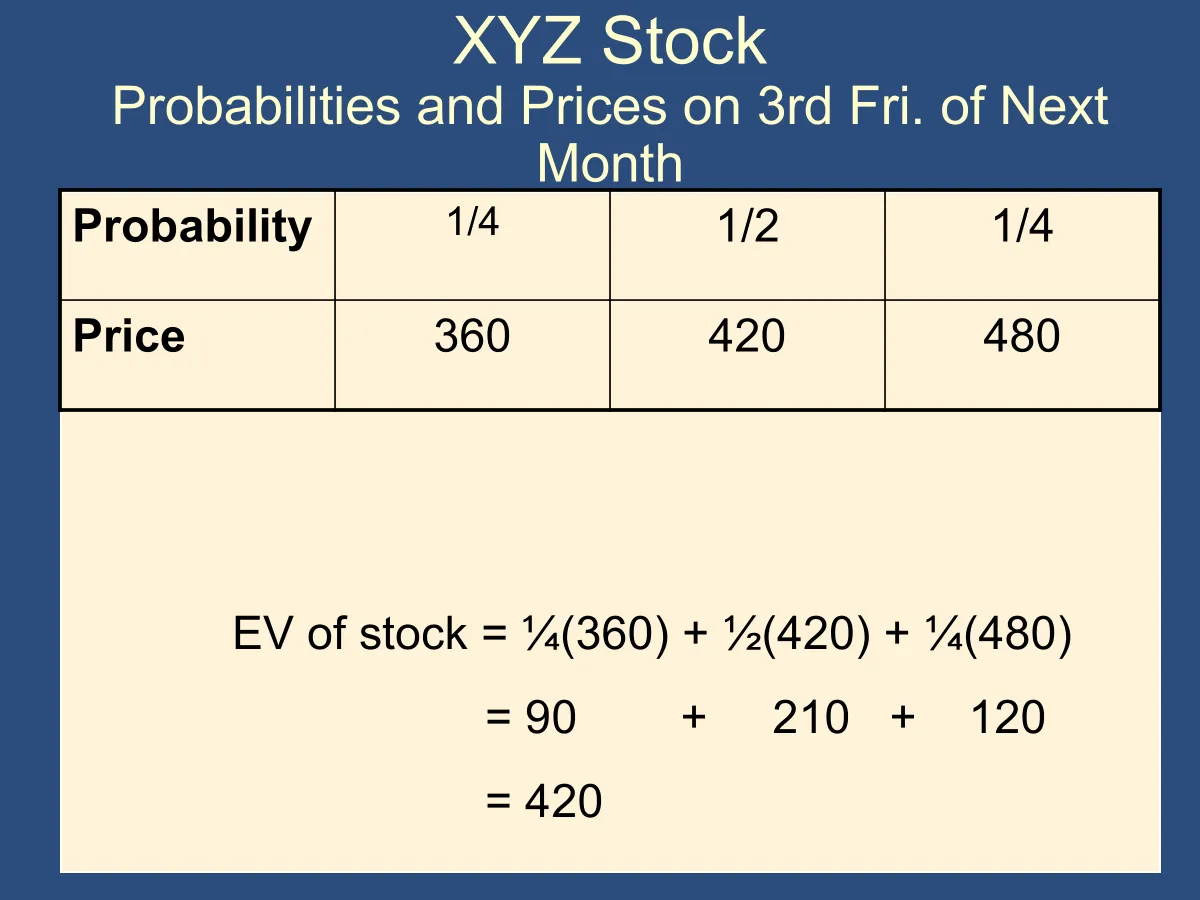

To find the price of a stock, calculate the EV of it’s future price:

You do not need to calculate the present discounted value of the expected value if you are not predicting very far in advance. If you are just calculating the stock’s expected value in a month, there is no point in taking the present discounted value because you are not discounting for much time. Similarly, if you are not expecting a dividend next month, you do not need to include the dividend term.

What we are doing here (using the expected value to calculate the stock price) is a special case of what we learned when we covered the EMH.

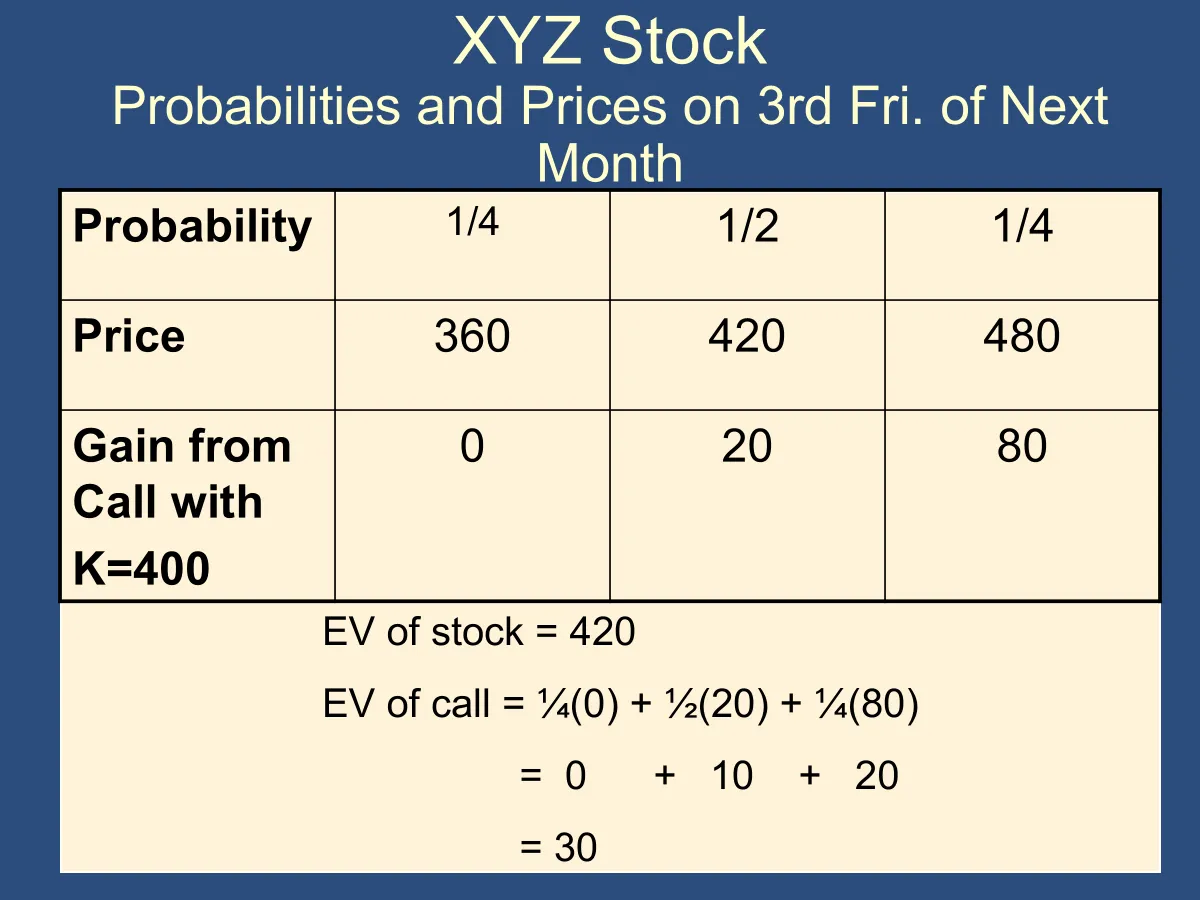

To calculate the premium of a call or put, just take the EV of the gain you could make based on the market’s expectation of the future stock prices at expiration:

You can use the same approach with any option strategy you’re considering. Think about the potential gains or losses at expiration from the positions in the strategy. That will tell you what the net premium of the strategy should be.

| Outcomes | Good | Bad | OK |

|---|---|---|---|

| S at Expiration | 100 | 80 | 90 |

| Probability | 30% | 30% | 40% |

| How much is the stock worth? | |||

| How much is a k=$80 call worth? | |||

| How much is a k=$80 put worth? |

| Outcomes | Good | Bad | OK |

|---|---|---|---|

| S at Expiration | $100 | $80 | $90 |

| Probability | 30% | 30% | 40% |

| Gain from $80 call | $20 | $0 | $10 |

| Gain from $80 put | $0 | $0 | $0 |

| Price of Stock = EV of Stock = 30%×$100 + 30%×$80 + 40% ×$90 = $90 | |||

| Premium of $80 call = EV of Gain from $80 call = 30%×$20 + 30%×$0 + 40% ×$10 = $10 | |||

| Premium of $80 put = EV of Gain from $80 put = 30%×$0 + 30%×$0 + 40% ×$0 = $0 |

| Outcomes | Good | Bad | OK |

|---|---|---|---|

| S at Expiration | $100 | $80 | $90 |

| Probability | 30% | 30% | 40% |

| Gain from $80 call | $20 | $0 | $10 |

| Gain from $80 put | $0 | $0 | $0 |

| Long Straddle | $20 | $0 | $10 |

| Premium of Straddle = EV of gain from straddle = 30%×$20 + 30%×$0 + 40% ×$10 = $10 |

🕣

❔ Help me understand time value?

✔ The value of a put or a call comes from the fact that you can exercise it and make money. You can estimate how much you could exercise an option today using the intrinsic value formula, so intrinsic value is the foundation of an option’s overall value. Options typically sell for more than their intrinsic value. The extra premium you pay above the intrinsic value is called the time value. Time Value = Premium - IV the time value is typically positive because people are willing to pay more than the option’s intrinsic value. They can afford to wait and exercise the option later, after they see whether the stock goes up or down. Since they do not have to decide whether to exercise it immediately, the option is worth more today, which is why the premium is usually higher than the intrinsic value.

🕣 5:04pm

❔ Interpretation question - If the number of shares in 1 contract is not given, should we assume that 1 contract is worth a 100 shares - based on the standard options contract?

✔ yes

🕣 5:04pm

❔ Stock options in compensation packages.

✔ A stock option in a compensation package is a contract between the firm and the employee that lets the employee buy shares at a set price on or after a certain date, subject to certain conditions. It is similar to a market-traded option, but employee stock options are not traded on an exchange.

Employee stock options can be written differently. You cannot trade your compensation on an exchange, so you also cannot trade an employee stock option on an exchange. Often, employee stock options look more like warrants. A warrant is similar to an option, but the firm agrees to create new shares so you can buy them.

Employee stock options are usually call options. A call option lets you buy a share of the stock at a locked-in price, rather than buying it from someone else (i.e., from the short side of the contract). Instead, you buy a newly created share from the firm. The firm can always issue additional shares, but it usually needs a board vote to do so.

Board votes (or even investor votes) are important in compensation plans that involve options. They typically identify a block of authorized shares and set aside those shares for issuance when the employee exercises the option. When the employee exercises, the firm takes those authorized shares out of the authorized pool and adds them to the issued shares (shares outstanding), consistent with the contract terms. There can be variations in the contract as well.

🕣 5:07pm

❔

If I have to buy 1 contract at a cost of $2 per share, then for me to calculate the total price for the 1 contract do i assume its 100 shares.

Hence the total cost will be 2*100 = 200?

✔ Yes!

🕣 5:8pm

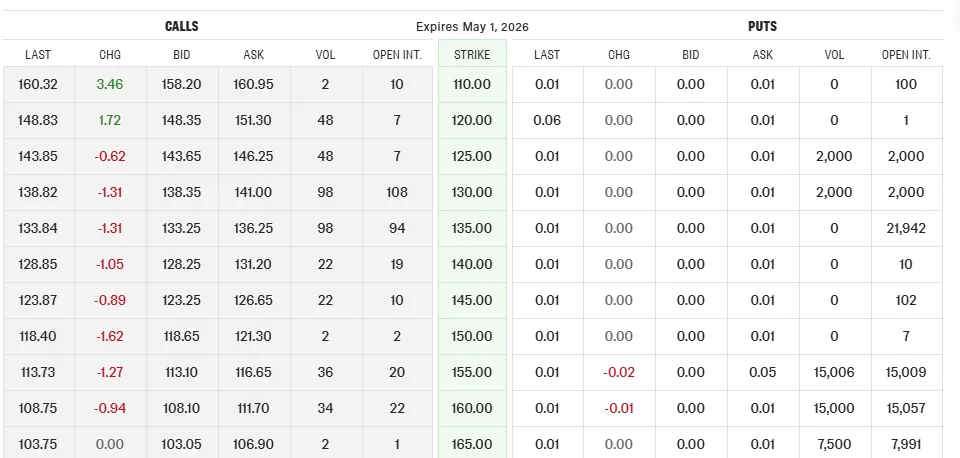

❔ Also if I have a table like below - what does the Last column imply - is this the premium?

✔ The short answer is that when Bruce asks for the premium of an option, he usually means the cost of buying the option on a per-share basis. For example:

- Question 1a: He is asking for the per-share premium.

- Question 1b: He is asking for the total cost to buy one entire contract.

I will cover the meaning of the last column in the section, but the short answer is that it is where you should look when you are looking for premiums for individual options (per share in this case). The premium you pay for an option depends on whether you are buying or selling. When you buy an option, you often pay the ask price. When you sell an option, you often pay the bid price. The detailed mechanics of how this type of market works are covered in a bit more depth in the second lecture on Equities. I brought it up then because we cover limit orders then, it is important, and I know it is helpful background now. Here is the page I used to accompany that part of the presentation: https://2000.robmunger.com/l9/etc/limitorders/ (Password=Watson)

The bid and ask are both limit orders resting on the exchange, waiting for someone to match them.

To avoid going into detail, Bruce has you look up the “last” column for all option premiums. That column shows the price that both the buyer and the seller paid in the most recent transaction. The “last” column may be a bit out of date, but at least you do not have to distinguish between the buyer and the seller.

I am happy to go into as much detail as you would like about this, or we can keep it short, whichever you prefer.

📅 Questions covered Tuesday, May 5 NOON

Section titled “📅 Questions covered , May 5 NOON”🕣 12:15pm

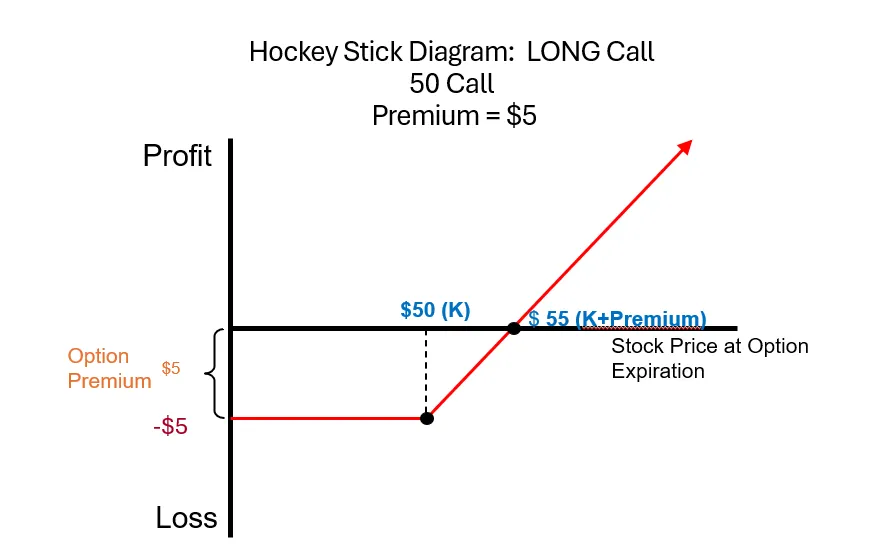

❔ I’m trying to ensure that I’m drawing and interpreting the hockey stick diagrams correctly. So I made up some questions and numbers below and plotted them. Would you please confirm if the below are correct.

Q1 : Draw a Hockey Stick Diagram for a Long Call that shows the PL

- K = 50

- Premium= 5

- K + Premium = 55

- S =45

- PL = MAX (S-K,0) - PR = $0 -$5 = -$5

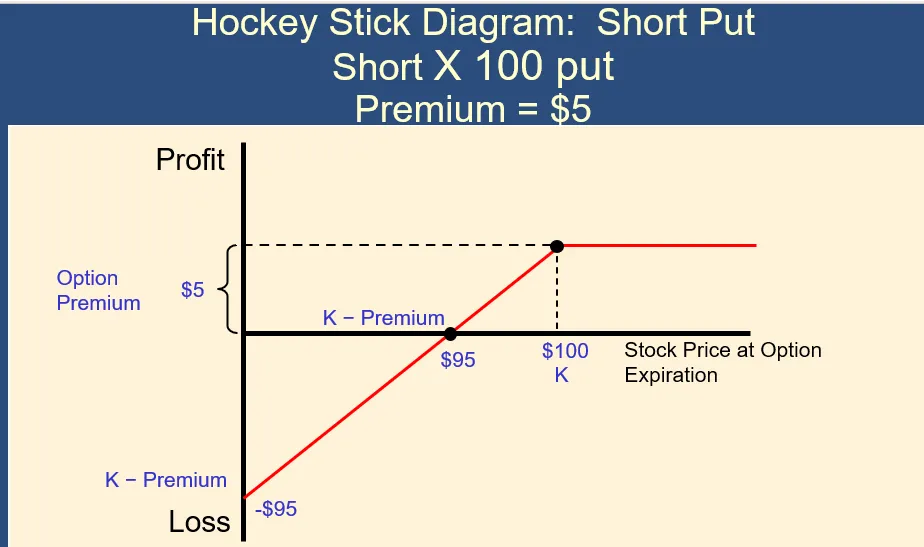

Q 2 : Draw a Hockey Stick Diagram for a Short Put that shows the PL

- K = 100

- Premium = 5

- K- Premium = 95

- S =110

- PL = $5

✔ Both look great

🕣 12:20pm ish

❔

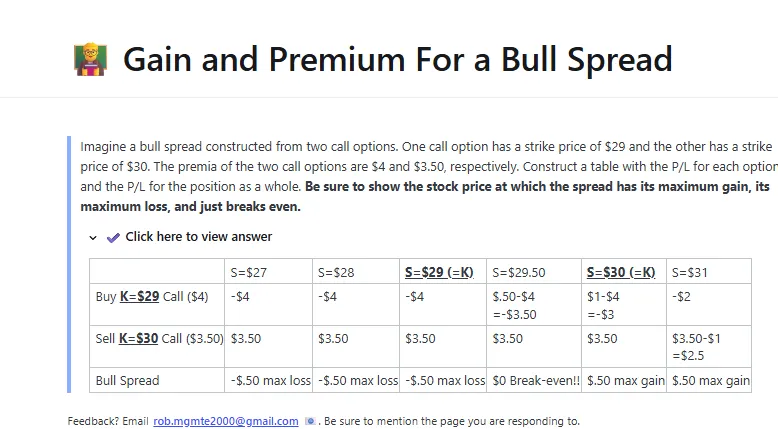

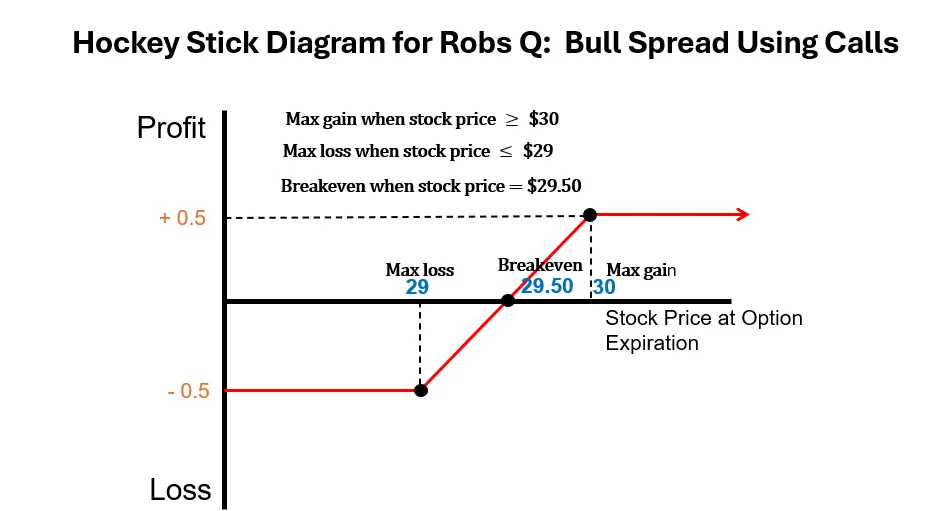

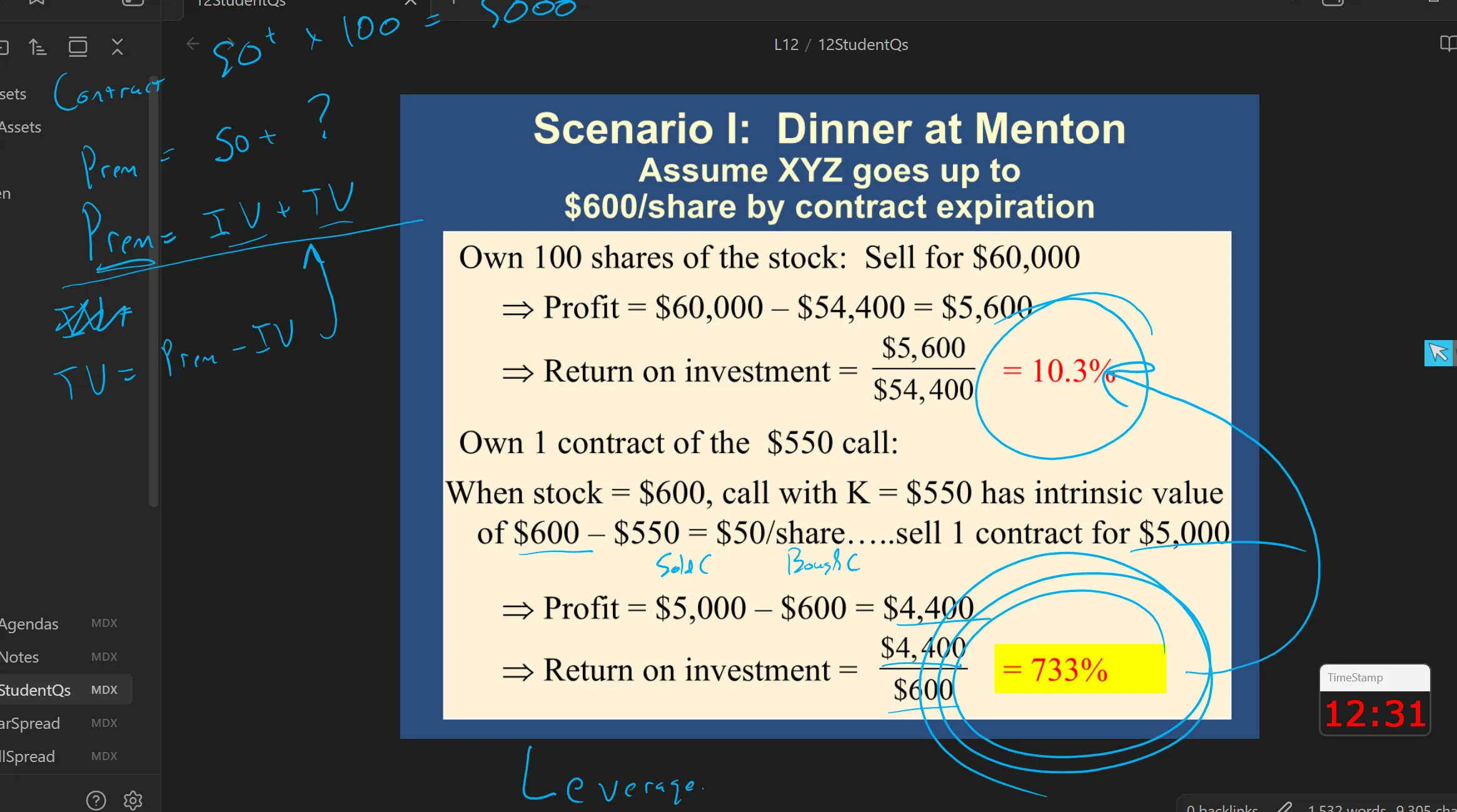

Q3- From a question on your Lecture 12- Option Strategy > Gain and Premium For a Bull Spread. You did not provide a diagram on this so I attempted to create one that shows the PL as well. Would you please confirm that I’m on the right track? https://2000.robmunger.com/l12/gainandpremiumforbullspread/

✔

🕣 12:25pm

❔

✔

🕣 12:32pm

❔ What proportion theoretical on exam?

✔

🕣 1:09pm

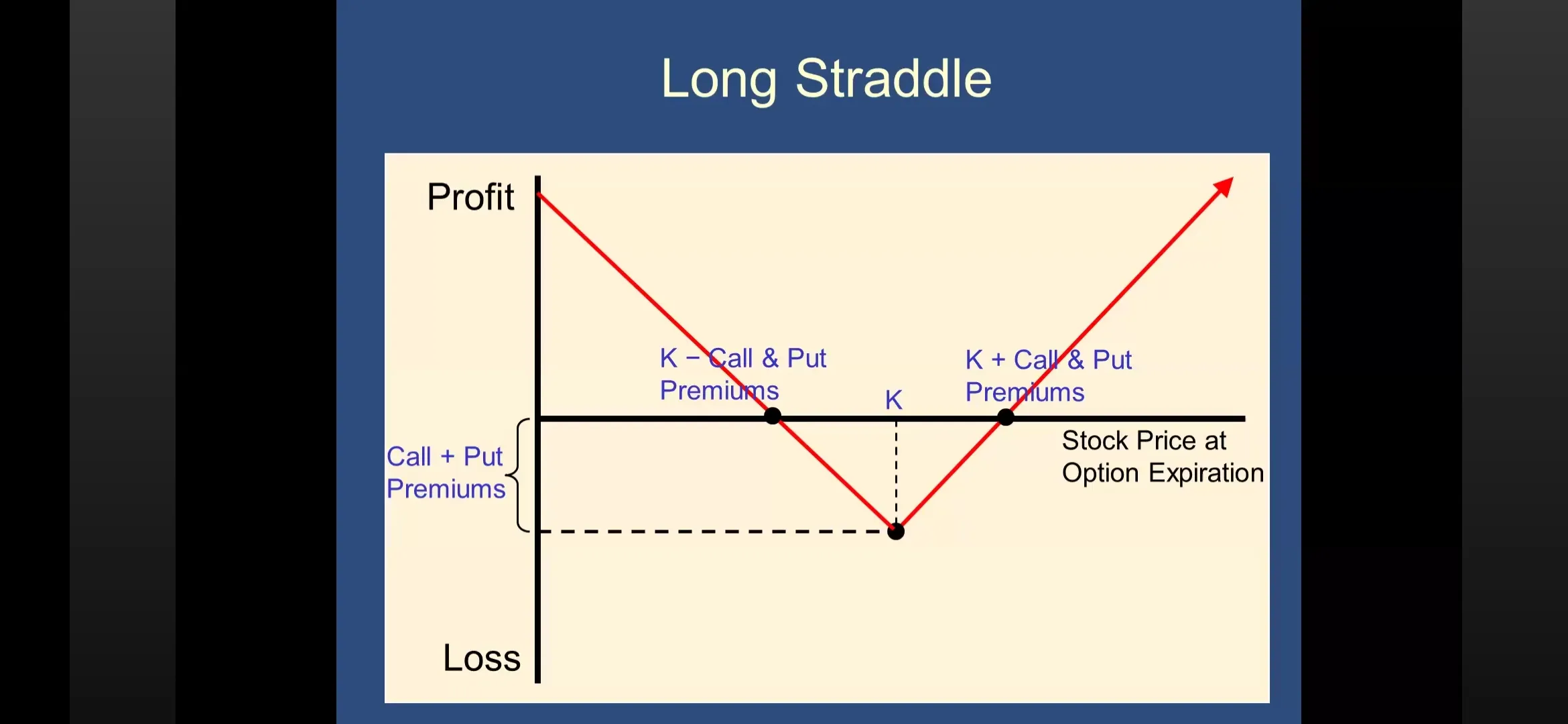

❔ 1.a. I understand Prof. Watson recommends Long Straddle, and I think this strategy is great.

Seeing the current market situation, do you think long straddles are a good strategy for crypto option trades or for bubble stocks like SanDisk due to their high volatility? (I’m not seeking financial advice just in case.)

I see crypto such as BTC, ETH, SOL have a tendency to not stay in a range due to their high volatility, and predict NAND stocks like SanDisk are currently in a bubble that they will keep going up or crash soon.

✔ This strategy is attractive because you can win whether the stock goes up or down. That said, whether a strategy makes sense depends on the probabilities you expect and whether you think the stock will be in the areas where you make money or the areas where you lose money.

You can still lose money using any specific option strategy. I’m sure you know this, but I want to emphasize that, from my perspective, the attractiveness of a strategy also depends on the premium and your investing thesis. Those are important factors.

See recording.

🕣 1:15pm

❔ 1.b. If so, I wonder why most of the traders I see online, both in the world and in Japan, don’t seem to take this strategy. Most of the influencers just don’t know the strategy as they aren’t professionals, or there’s a drawback that I’m missing?

✔ This is the point that I was making above, that it comes down to the premium. You need to have an insight that the rest of the market doesn’t have. Sometimes you want to be “long volatility” with a long straddle (if you think the market is underestimating volatility). Sometimes you want to be “short volatility” with a short straddle (if you think the market is overestimating volatility).

🕣 1:16pm

❔ 2. I really liked the lectures about the trades, such as technical, behavioral, theoretical, and option techniques. I’m currently interested in trades and possibly quantitative analysis. I wonder which courses you recommend me to take to advance the materials we covered in this course and the fields I mentioned above at DCE (or websites outside of the school).

✔ You might consider E 1920, Capital Markets and Investments, which Bruce teaches in the fall (I help). It builds on this course and can be thought of as “part 2” of this course.

We also teach a similar course to 1920 in the summer, 1452, Money, Financial Institutions, and Markets, but that is an summer course (intensive - twice as much work per week), so it might be too much. It might also be better to take it after 1920 because summer courses are “intensive.”

🕣 1:21pm

❔ Quick question about the problem sets. In questions 1a and 1d we have to determine option premium or use option to derive time value respectively.

Given the picture of the options chain provided, there is a enough info to use a method to derive the option premium. However, we’re actually given the ask and bid pricing. Neither of those methods are guaranteed to provide actual options pricing e.g. an order for options could not be fulfilled if there is not sufficient liquidity at that moment, and estimating options premiums based on gamma, delta, etc does not necessarily exactly reflect what people are willing to pay for the option.

Do we use the data provided, or should we try to approximate using methods that seem outside the scope of this class. I think I know the answer but not sure if I missed something because the chart in the question on the problem set is different than what we covered in lecture and the website. It provides enough data to derive EV and IV.

✔ In Bruce’s classes, you should not use any material from outside the class. Each class is self-contained, so he will give you everything you need, so you do not need to worry about anything else.

If you look at the problem set, there is a note that says to use the last column for all option-pricing problems. For those, just use the last column to determine what the premium should be. We covered it on Saturday, and I am not sure if you had a chance to watch the Saturday section, but we go into detail there. Just use the column labeled “Last.” I will show you.

In real-life trading, the last column shows the price at which the last trade was executed.

- The bid is the price people are bidding for the option. It is the price they will pay to buy it.

- If you want to sell, you sell at the bid, because someone is willing to buy it at that price right now.

- The ask is the price people are offering to sell it for. If you want to buy, you buy at the ask.

- The last is the actual price of the last transaction.

Bid means “I will bid $100 to buy your stock” Ask means “I will sell you the stock, but I ask for you to pay me $101.” Both of the above are limit orders.

- There is a limit buy order for $100 (someone is bidding $100)

- There is a limit sell order for $100 (someone is asking $100)

If I want to buy, I need a seller. Therefore, I need to know what people are asking. Ie.

- I want to buy, and someone else is asking me to pay $101, so if I want to buy, I pay $101.

- I want to sell, and someone else is bidding $100 for my stock, so if I want to sell now, I receive $100.

🕣 1:33pm

❔ I wanted to ask whether the final exam will have a similar time structure to the midterm. I found myself running out of time on the midterm, and I’m trying to prepare more effectively this time around. With the problem sets, I’m able to spend as much time as needed on each question, so I tend to do well, but under time pressure during exams I sometimes struggle with anxiety.

✔ As mentioned earlier today, I posted a review session where I go over a lot of your concerns. The most important thing to keep in mind is that the more you practice and study, the more these skills will become second nature. There is not a huge range in the types of skills being asked on these exams. For all of Bruce Watson’s classes, the material you need to know is fairly circumscribed. To stay on track:

- Do all the practice problems on my website.

- Redo the homework problems.

- If there are specific areas where you want more practice to get faster, shoot me an email and tell me which ones you’re stuck on, and I’ll help with those.

- I’ll also be posting more resources throughout the week if I can. Practice makes perfect!

🕣 1:35pm

❔

I also had a quick logistical question. On this week’s problem sets, we are asked to draw graphs. Will that be required on the final as well? If so, would it be acceptable to draw them by hand and upload them during the exam? I typically scan or email them to myself before uploading, so I wanted to confirm whether switching between applications (like email) during the test is allowed.

✔ We do not know whether there will be any diagrams on the exam. If there are, we will give you a little extra time for them. You can scan them so you do not spend too much time. If you need to, it is fine to:

- Do the diagrams by hand.

- Take a photo of them.

- Upload the photo to your email.

That is how I would do it. We are pretty laid-back, we are on your team, and we can tell you are honest.

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.