Formulas will be added to this page as they are covered in class. The formulas are grouped by lecture, and each lecture has a link to the relevant lecture notes.

Press Ctrl-D to bookmark this page. A downloadable paper/Microsoft Word formula sheet can be found in my File Share.

Questions or comments? Please email rob.mgmte2000@gmail.com. Remember, your first reference is always the lectures and the homework. Feel free to download my materials, but please do not reupload them.

In some of the right-hand examples columns, I write formulas in "spreadsheet-style." '*' represents multiplication and '^' represents exponents.

Formulas will be added to this document after Bruce has introduced them in class.

L2 - Money and Banks

Section titled “ L2 - Money and Banks”Bruce often refers to M1 as the “Money Stock” or the “Money Supply.”

Definition of Bank Capital:

With algebra, this implies that the left and right of balance sheet are equal: ️⚖️

Bruce’s 6 Bank Balance Sheet Event Examples are helpful.

References: 2 Feb 3.ppt and L2-Bank Balance Sheets

L3 - Bank Profitability and Leverage

Section titled “ L3 - Bank Profitability and Leverage”10% = 1% × 10

L3 - Reserves

Section titled “ L3 - Reserves”“Deposits at Fed” = "Deposits at the Central Bank"

L3 - Bonus Reserves Equations

Section titled “ L3 - Bonus Reserves Equations”Occasional questions may ask you to reason about excess and required reserves. With a tiny bit of algebra, these nine equations follow from what you’ve learned in class. I lay them out here systematically for reference. ( means “Dollars of Required Reserves,” etc.)

| Required Reserves Version | Excess Reserves Version | Required and Excess | |

|---|---|---|---|

| To find: R or E | |||

| To find: $Reserves | |||

| To find: Deposits |

L3 - Money Multiplier

Section titled “ L3 - Money Multiplier”References: 3 Feb 10.ppt and L3-Measures of Bank Profitability

L4/L5 - Monetary Policy

Section titled “ L4/L5 - Monetary Policy”You can use the two green equations, above, for Deposits/Withdrawals and Open Market Operations. For an Open Market Operation, . If I deposit $10, (if I withdraw $10 ).

References: 4 Feb 17.ppt and L4-Reserves

and

(=real interest rate; =nominal interest rate; =inflation rate)

References: 5 Feb 24.ppt and L5-Outline

L6 - NPV and IRR

Section titled “ L6 - NPV and IRR”In spreadsheet notation, you write, FV = PV*(1+i)^N and PV = FV/(1+i)^N

Present Value of a stream of payments for T years:

To enter the above formula as plain text, write: PV = PMT1/(1+i)^1 + PMT2/(1+i)^2 PMT3/(1+i)^3 + ... + PMTT/(1+i)^T

To solve an IRR problem, write down NPV=0 or PVInflows = PVOutflows and solve for i.

NPV Rule: Undertake any project with a positive NPV. If two mutually exclusive projects have positive NPV, undertake the project with the higher NPV. (NPV is like the profit of the project.)

IRR Rule: Undertake any project for which the IRR is greater than the opportunity cost of capital.

References: 6 Mar 3.ppt and L6-Outline

Midterm

Section titled “ Midterm”L7 - Bonds

Section titled “ L7 - Bonds”F=Face value; T=Number of years until bond expires; i=discount rate/Interest rate; c=Coupon rate; Fc=F×c=a single coupon payment

For a 3 year coupon bond:

Plain Text Formulas:

- 2 Year Coupon Bond:

PB = Fc/(1+i)^1 + (Fc+F)/(1+i)^2 - 3 Year Coupon Bond:

PB = Fc/(1+i)^1 + Fc/(1+i)^2 + (Fc+F)/(1+i)^3 - T Year Coupon Bond:

PB = Fc/(1+i)^1 + Fc/(1+i)^2 + Fc/(1+i)^3 + ... + (Fc+F)/(1+i)^T - Zero Coupon Bond:

PB = F/(1+i)^T

Shortcut to calculate price of a 4 year coupon bond with F=$1000, i=8%, and c=6%: (Note that Fc = $60)

PB = 60/1.08 + 60/1.08^2 + 60/1.08^3 + 1060/1.08^4

To solve a Yield To Maturity (YTM) problem, write down the bond pricing formula and solve for i.

| ⇔ | ⇔ | “Discount Bond” | ||

| ⇔ | ⇔ | “Par Bond” | ||

| ⇔ | ⇔ | “Premium Bond” |

References: 7 Mar 24.ppt, L7-Outline, and L7-Notes

L8/L9 - Stocks & Investment Companies

Section titled “ L8/L9 - Stocks & Investment Companies”Authorized Shares = Issued Shares + Unissued Shares

Issued Shares = Shares Outstanding + Treasury Stock

Shares Outstanding = Float + Restricted Shares

My “Classes of Shares” worksheet can you help solve problems using the above equations.

Market Capitalization: Market “Cap” = Shares Outstanding × Price Per Share

References: 8 Mar 31.ppt, L8-Outline, L8 Notes, 9 Apr 7.ppt, and L9 Notes

L10 - CAPM and EMH

Section titled “ L10 - CAPM and EMH”CAPM:

CAPM Jargon:

Expected return (required by the market) for a portfolio or individual stock

= Expected return for/of the market portfolio

= risk free rate = rate on return of assets considered to be risk-free = return on T-Bills

“Risk Premium” means you subtract off the risk free rate.

= Market risk premium = Expected risk premium of market

= Probability of Outcome 1 × Value of Outcome 1

+ Probability of Outcome 2 × Value of Outcome 2

+ Probability of Outcome 3 × Value of Outcome 3

+ …

+ Probability of Outcome N × Value of Outcome N

EMH stock price = PDV of EV of future price + PDV of dividend

Example:

Stock price =

Stock price =

References: 10 Apr 14.ppt and L10 Notes

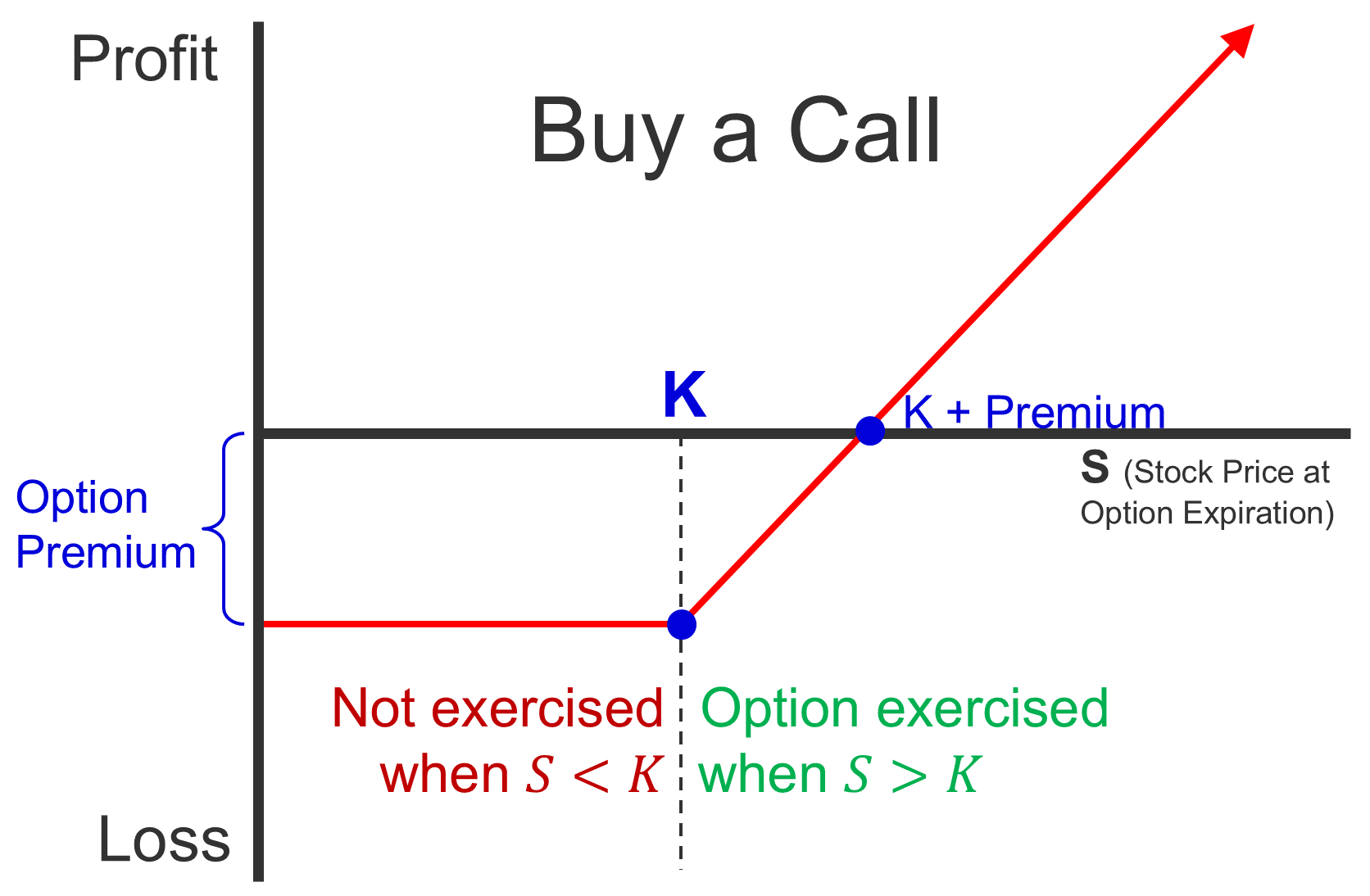

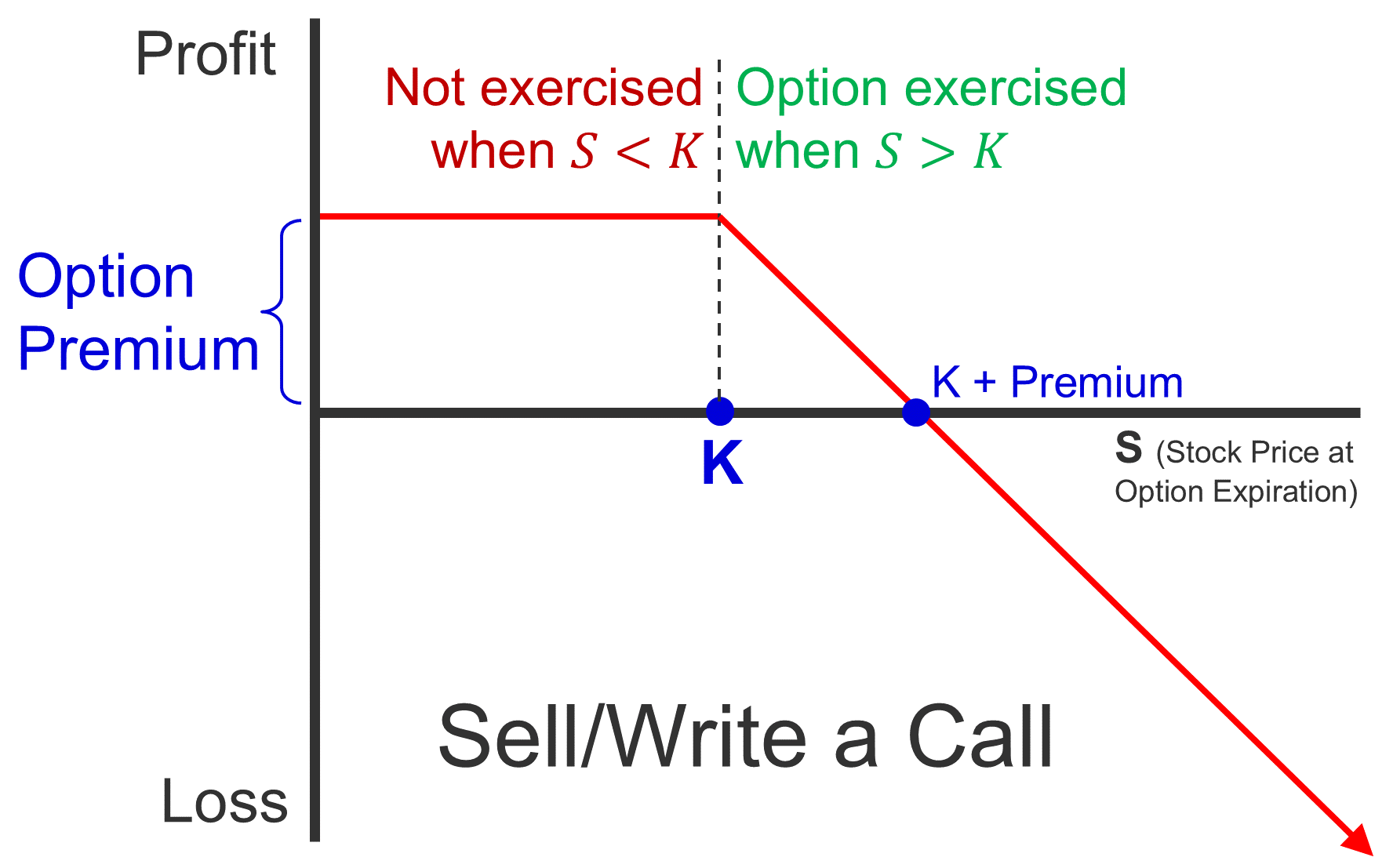

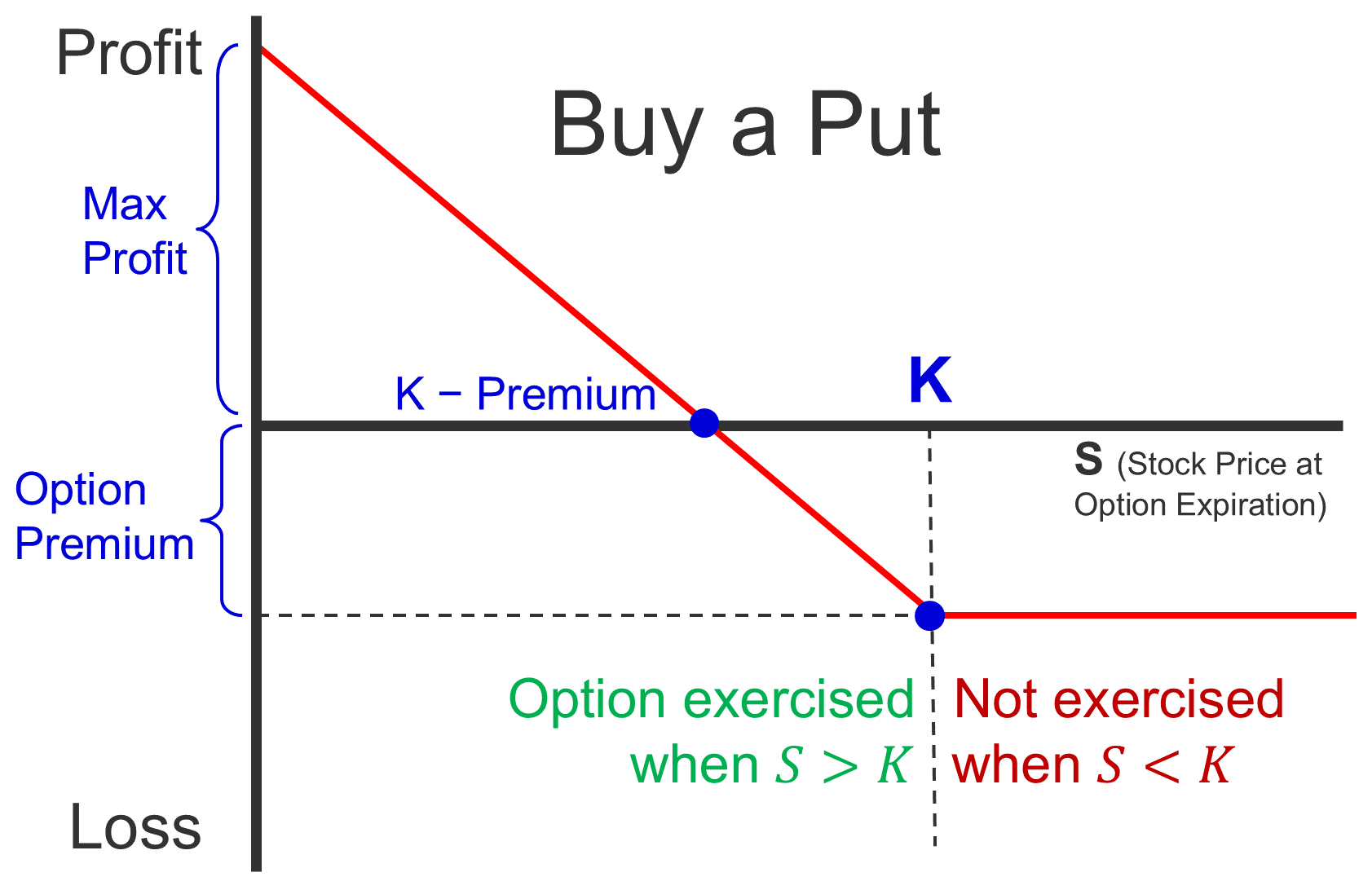

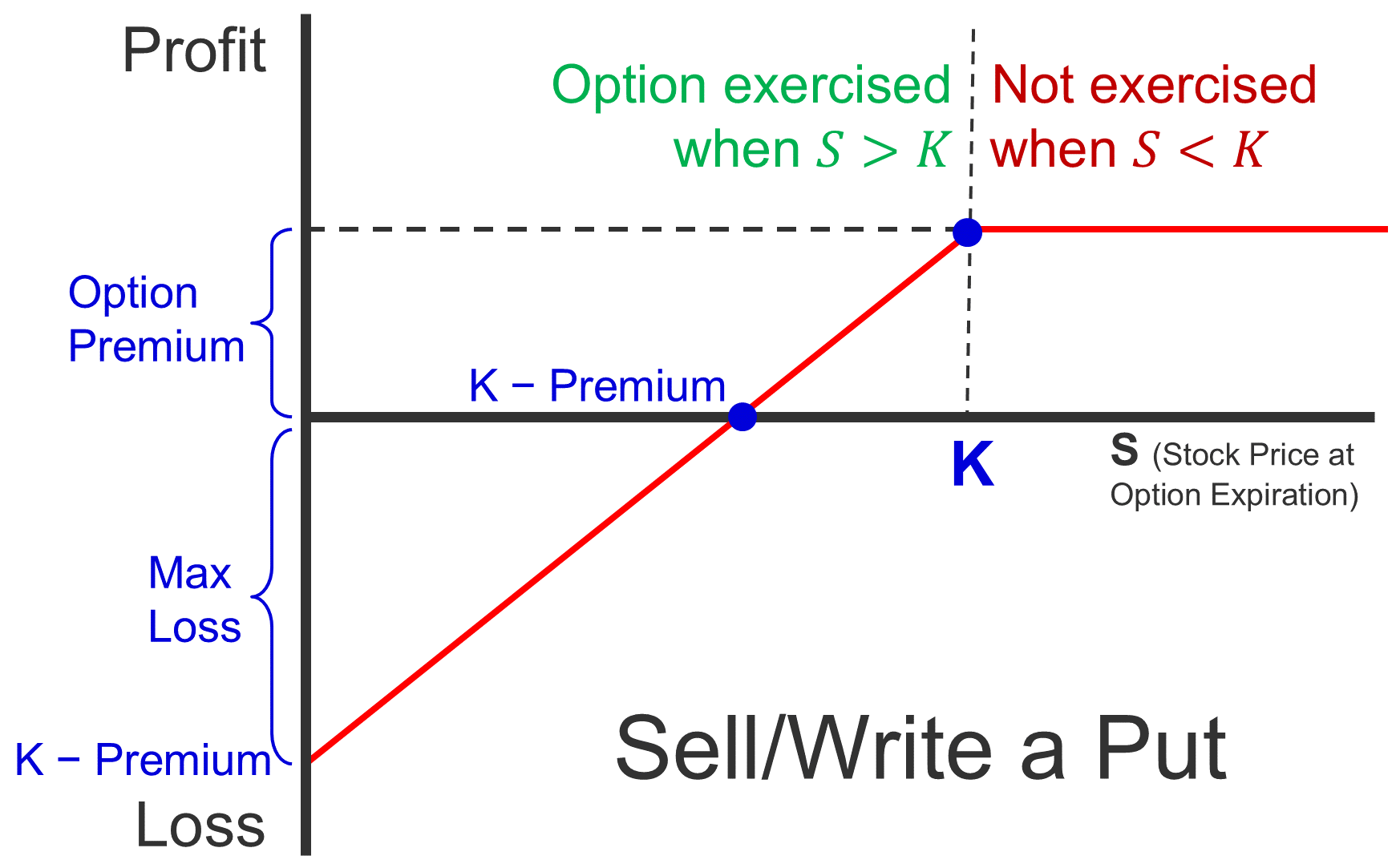

L11 Options

Section titled “ L11 Options”② P/L Formulas:

P/L from Buying an Option

P/L from Selling an Option

Combining ① and ②:

P/L from Buying a Call

P/L from Buying a Put

P/L from Selling a Call

P/L from Selling a Put

Premium = Intrinsic Value + Time Value

Leverage = Share Price×100 / Premium×100

| Buy/Long | Write/Sell/Short | |

|---|---|---|

| Call |  |  |

| Put |  |  |

References: 11 Apr 21.ppt and L11 Notes

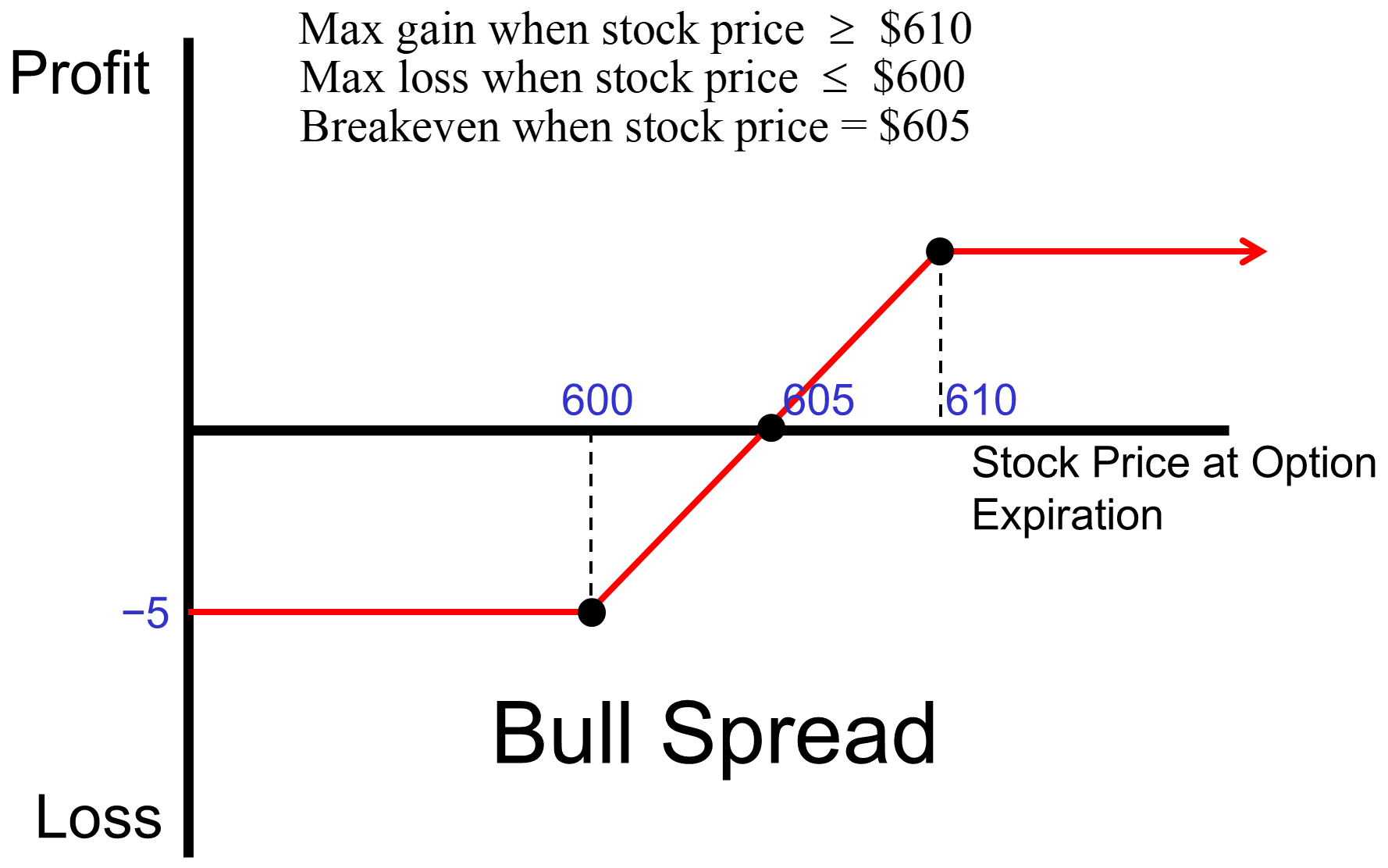

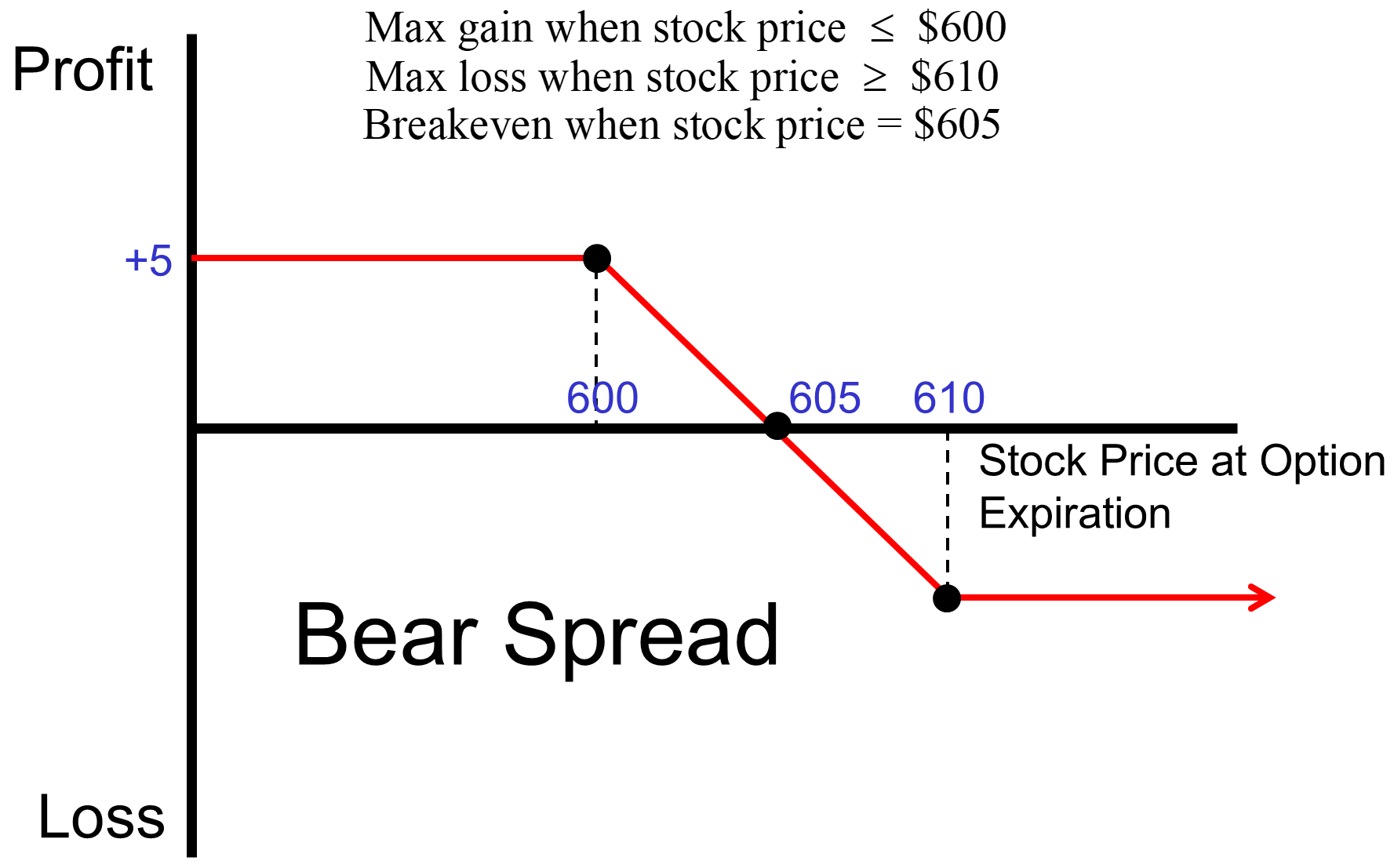

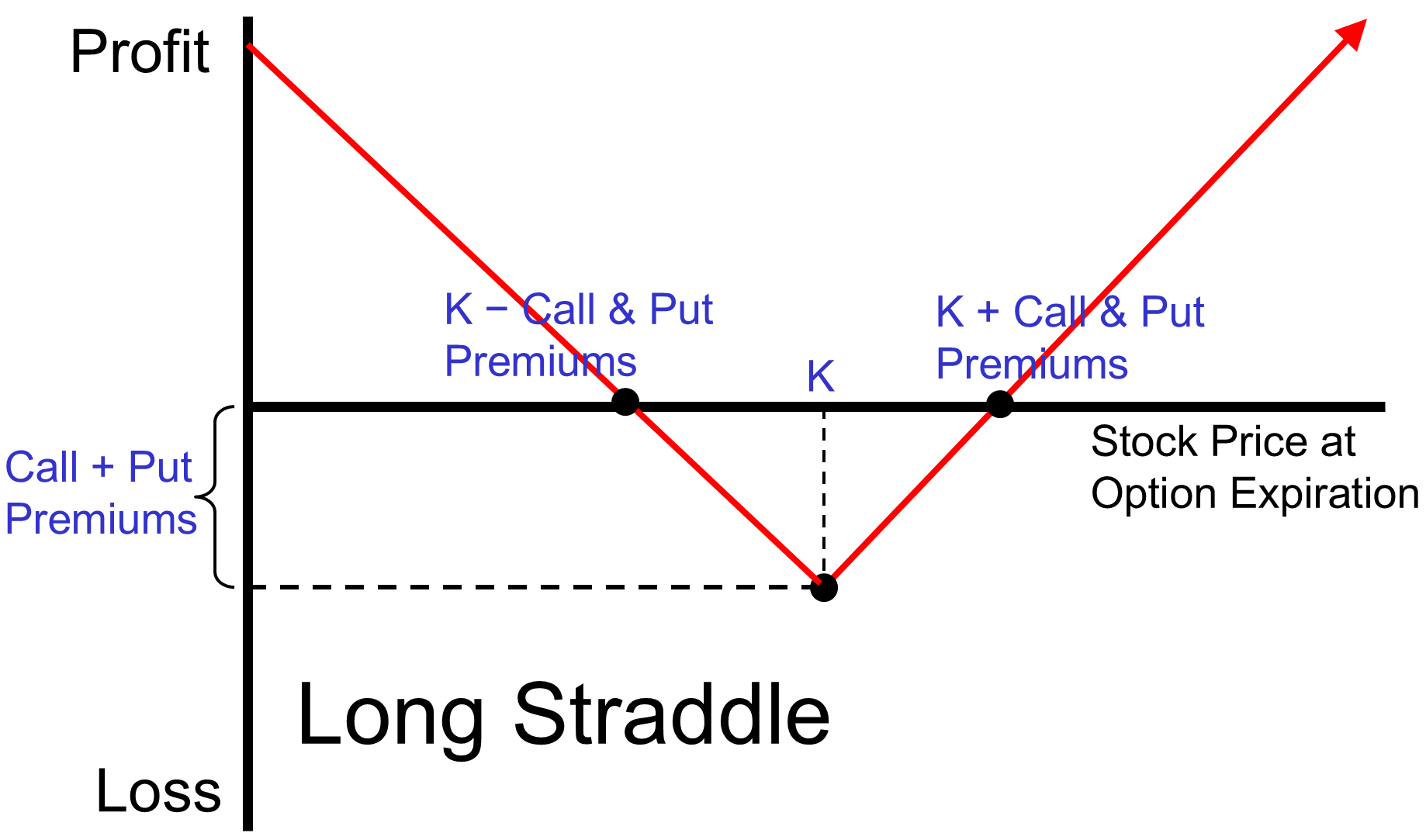

L12 Options Strategies

Section titled “ L12 Options Strategies”| Spreads | Straddles |

|---|---|

A cheap, low risk bet that S will be relatively high. Construction: Buy a call with lower strike price and sell a call with higher strike price. |  A cheap, low risk bet that S will be relatively low. Construction: Sell a call with a lower strike price and buy a call with a higher strike price. |

A bet on high volatility. Construction: Buy a call and a put with the same strike price. |  A bet on low volatility. Construction: Sell a call and a put with the same strike price. |

References: 12 Apr 28.ppt, and L12 Notes

Futures

Section titled “ Futures”

Buy the contract:

Sell the contract:

(for example)

($250 for ‘full-sized contract,’ $50 for e-mini, and $5 for micro e-mini)

References: 13 Dec 2.ppt, L13 Notes

© 2026 Rob Munger

Feedback? Email rob.mgmte2000@gmail.com 📧. Be sure to mention the page you are responding to.